Efficiency effectiveness of PPh 21 reporting via taxation digitalization in state institutions using value for money

Article Sidebar

Main Article Content

Abstract

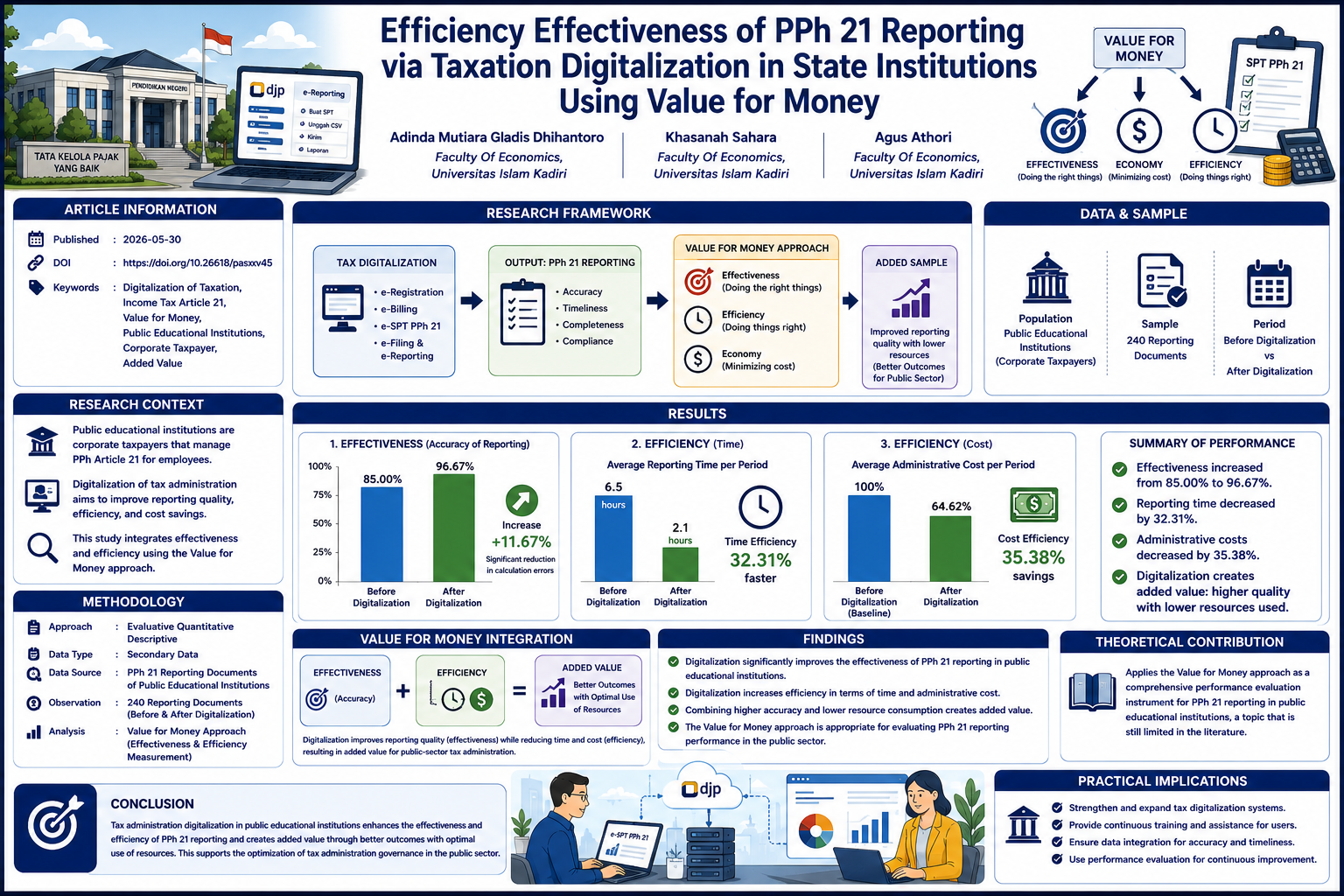

This research aims to analyze the impact of tax administration digitalization on the reporting performance of Income Tax (PPh) Article 21 in public educational institutions using the Value for Money approach. In contrast to previous studies that generally focus on individual taxpayer compliance or the private sector, this study positions public educational institutions as public-sector corporate taxpayers and integrates measurements of effectiveness and efficiency into a single, comprehensive evaluative framework. The study employs an evaluative quantitative descriptive approach based on 240 secondary administrative reporting documents, covering periods both before and after digitalization. The results indicate that digitalization increased reporting effectiveness from 85.00% to 96.67%, reflecting a significant reduction in calculation errors. From an efficiency perspective, the average reporting time decreased from 6.5 hours to 2.1 hours per reporting period, representing a time efficiency rate of 32.31%, while administrative costs decreased by 35.38%. The integration of increased accuracy and reduced resource consumption demonstrates that digitalization not only improves reporting quality but also creates added value in public-sector tax administration governance. The contribution of this research lies in the application of the Value for Money approach as a performance evaluation instrument for PPh Article 21 reporting within the context of digitalization in public educational institutions, an area that remains limited in the literature. These findings offer theoretical implications for the development of public-sector tax performance evaluation and practical implications for optimizing government tax digitalization policies.

Downloads

Article Details

Section

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

Bastian, I. (2021). Akuntansi Sektor Publik. Jakarta: Erlangga.

Direktorat Jenderal Pajak. (2016). Peraturan Direktur Jenderal Pajak Nomor PER-16/PJ/2016 tentang Tata Cara Pemotongan, Penyetoran, dan Pelaporan Pajak Penghasilan Pasal 21. Jakarta: DJP.

Direktorat Jenderal Pajak. (2022). Modernisasi Sistem Administrasi Perpajakan. Jakarta: Kementerian Keuangan Republik Indonesia.

Direktorat Jenderal Pajak. (2024). Coretax Administration System. Jakarta.

Direktorat Jenderal Pajak. (2024). Modernisasi Administrasi Perpajakan. Jakarta.

Ghozali, I. (2018). Aplikasi Analisis Multivariate dengan Program IBM SPSS. Semarang: Badan Penerbit Universitas Diponegoro.

Halim, A., & Kusufi, M. S. (2014). Akuntansi Sektor Publik. Jakarta: Salemba Empat.

Kementerian Keuangan Republik Indonesia. (2007). Undang-Undang Nomor 28 Tahun 2007 tentang Ketentuan Umum dan Tata Cara Perpajakan. Jakarta.

Kementerian Keuangan RI. (2023). Laporan Kinerja DJP. Jakarta.

Lestari, N., & Dewi, P. (2022). Digitalisasi layanan perpajakan dan kepatuhan wajib pajak. Jurnal Riset Akuntansi.

Mahmudi. (2019). Manajemen Kinerja Sektor Publik. Yogyakarta: UPP STIM YKPN.

Mardiasmo. (2019). Perpajakan. Yogyakarta: Andi Offset.

Nugraha, T. (2023). Digitalisasi pajak dan efisiensi administrasi sektor publik. Jurnal Perpajakan Indonesia.

Nurhayati, E., & Hidayat, A. (2020). Pengaruh penerapan sistem administrasi perpajakan modern terhadap kepatuhan wajib pajak. Jurnal Akuntansi dan Keuangan Publik, 7(2), 85–96.

OECD. (2023). Digital Transformation in Tax Administration. Paris.

Pratama, Y. (2024). Implementasi Coretax dalam administrasi perpajakan Indonesia. Jurnal Perpajakan Modern.

Putri, R. A., & Pratama, A. (2021). Efektivitas dan efisiensi pelaporan pajak berbasis elektronik pada sektor publik. Jurnal Akuntansi Pemerintahan, 5(1), 45–58.

Rahmawati, L. (2022). Analisis efisiensi administrasi perpajakan berbasis digital. Jurnal Administrasi Negara.

Republik Indonesia. (2008). Undang-Undang Nomor 36 Tahun 2008 tentang Pajak Penghasilan. Jakarta.

Resmi, S. (2023). Perpajakan Teori dan Kasus. Jakarta.

Siregar, B. (2017). Akuntansi Sektor Publik. Yogyakarta: UPP STIM YKPN.

Sugiyono. (2019). Metode Penelitian Kuantitatif, Kualitatif, dan R&D. Bandung: Pratama, Y. (2024). Implementasi Coretax dalam administrasi perpajakan Indonesia. Jurnal Perpajakan Modern. Alfabeta.

Waluyo. (2022). Perpajakan Indonesia. Jakarta.

World Bank. (2022). Digital Government and Tax Reform.

World Bank. (2022). Digital Government and Tax Reform.