Optimizing PBB-P5L Revenue in the Mineral and Coal Sector through Business Process Analysis at KPP Pratama Batulicin

Article Sidebar

Main Article Content

Abstract

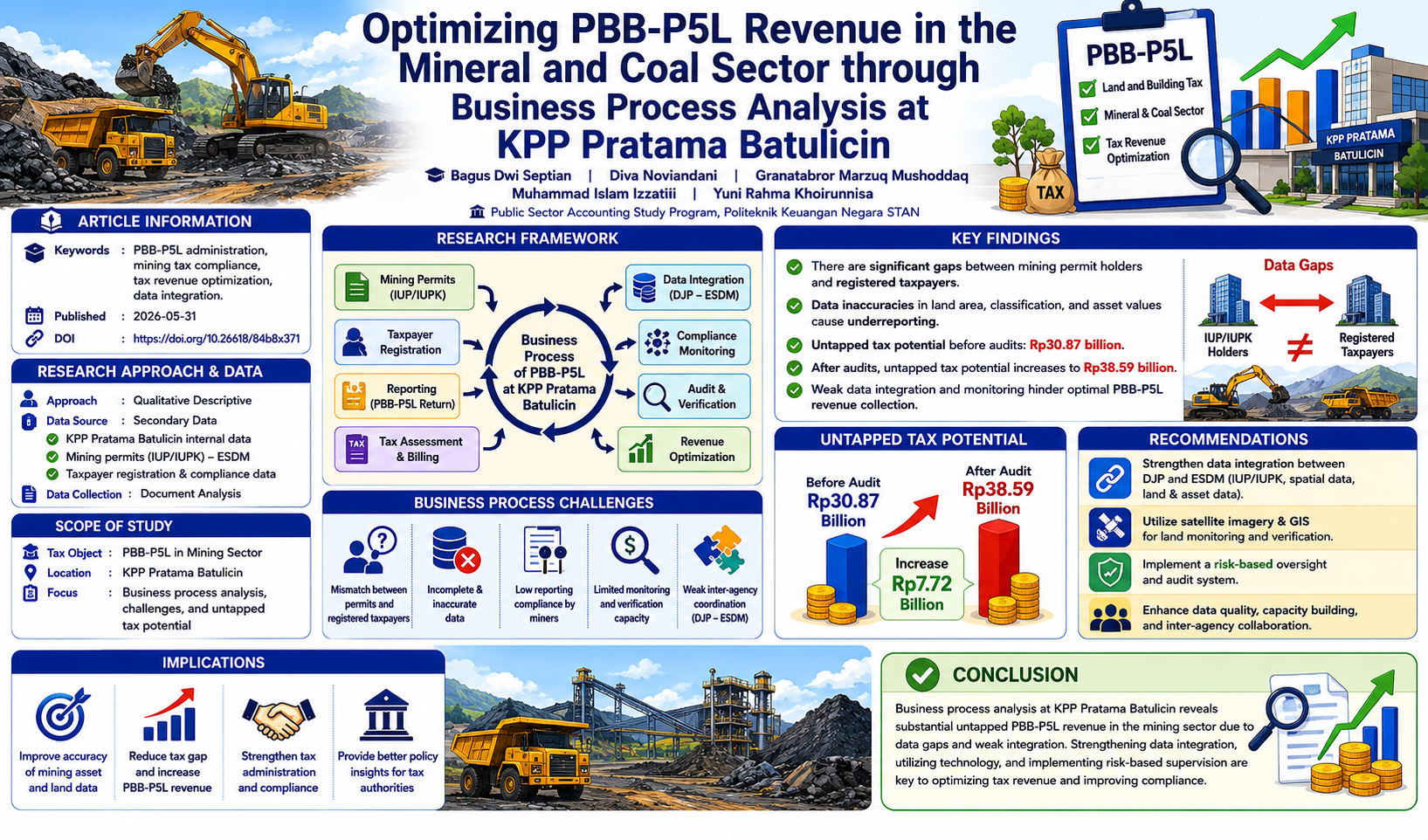

This study investigates the Business Process of Land and Building Tax (PBB-P5L) in the mining sector (minerba) at KPP Pratama Batulicin, focusing on the challenges that hinder optimal tax revenue collection. The primary objective is to examine how well the tax process operates, identify issues related to tax administration, and assess the untapped tax potential. Using a qualitative descriptive approach, the study analyzes secondary data from KPP Pratama Batulicin and external sources, including data on mining permits (IUP/IUPK) and tax compliance. Data collection was done through document analysis, with a focus on mining tax registration, reporting, and assessment procedures. The findings reveal significant discrepancies between the number of mining permit holders and registered taxpayers, as well as data inaccuracies that prevent effective tax collection. The estimated untapped tax potential before audits was Rp30.87 billion, increasing to Rp38.59 billion after audits, indicating a significant underreporting of taxable assets. The study suggests improvements in data integration between DJP and ESDM, the use of satellite imagery for land monitoring, and the implementation of a risk-based oversight system. These recommendations are expected to improve data accuracy, reduce the tax gap, and enhance PBB-P5L revenue collection, offering valuable insights for policymakers and tax practitioners aiming to optimize tax administration in the mining sector.

Downloads

Article Details

Section

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

Allingham, M. G., & Sandmo, A. (1972). Income tax evasion: A theoretical analysis. Journal of Public Economics, 1(3–4), 323–338. https://doi.org/10.1016/0047-2727(72)90010-2

Alm, J. (2023). Tax compliance and administration in the digital era. Edward Elgar Publishing.

Aslett, J., González, G., Hamilton, S., & Pecho, M. (2024). Tax administration: Essential analytics for compliance risk management (Technical Notes and Manuals No. 2024/001). International Monetary Fund. https://doi.org/10.5089/9798400260063.005

Bird, R. M., Bahl, R., & McCluskey, W. J. (Eds.). (2022). Property tax in Asia: Policy and practice. Lincoln Institute of Land Policy.

Bjørneby, M., Alstadsæter, A., & Telle, K. (2021). Limits to third-party reporting: Evidence from a randomized field experiment in Norway. Journal of Public Economics, 203, 104512. https://doi.org/10.1016/j.jpubeco.2021.104512

Brockmeyer, A., Estefan, A., Ramírez Arras, K., & Suárez Serrato, J. C. (2021). Taxing property in developing countries: Theory and evidence from Mexico (NBER Working Paper No. 28637). National Bureau of Economic Research. https://www.nber.org/papers/w28637

Castro, J. F., Velásquez, D., Beltrán, A., & Yamada, G. (2022). The direct and indirect effects of messages on tax compliance: Experimental evidence from Peru. Journal of Economic Behavior & Organization, 203, 483–518. https://doi.org/10.1016/j.jebo.2022.09.022

Darmayasa, I. N., & Hardika, N. S. (2024). Core tax administration system: The power and trust dimensions of the slippery slope framework tax compliance model. Cogent Business & Management, 11(1), Article 2337358. https://doi.org/10.1080/23311975.2024.2337358

Dumas, M., La Rosa, M., Mendling, J., & Reijers, H. A. (2018). Fundamentals of business process management (2nd ed.). Springer. https://doi.org/10.1007/978-3-662-56509-4

Food and Agriculture Organization of the United Nations. (2023). Geospatial information for sustainable land administration. FAO.

Grote, M., & Wen, J.-F. (2024). How to design and implement property tax reforms (Technical Notes and Manuals No. 2024/006). International Monetary Fund. https://doi.org/10.5089/9798400288753.061

Kelly, R., White, R., & Anand, A. (2020). Property tax diagnostic manual. World Bank. https://openknowledge.worldbank.org/handle/10986/34129

Kirchler, E., Hoelzl, E., & Wahl, I. (2008). Enforced versus voluntary tax compliance: The slippery slope framework. Journal of Economic Psychology, 29(2), 210–225. https://doi.org/10.1016/j.joep.2007.05.004

Kementerian Keuangan Republik Indonesia. (2019). Peraturan Menteri Keuangan Nomor 186/PMK.03/2019 tentang Klasifikasi Objek Pajak dan Tata Cara Penetapan Nilai Jual Objek Pajak Pajak Bumi dan Bangunan.

Kementerian Keuangan Republik Indonesia. (2022). Peraturan Menteri Keuangan Nomor 234/PMK.03/2022 tentang Perubahan atas Peraturan Menteri Keuangan Nomor 186/PMK.03/2019 tentang Klasifikasi Objek Pajak dan Tata Cara Penetapan Nilai Jual Objek Pajak Pajak Bumi dan Bangunan.

Kementerian Keuangan Republik Indonesia. (2024). Peraturan Menteri Keuangan Nomor 81 Tahun 2024 tentang Ketentuan Perpajakan dalam Rangka Pelaksanaan Sistem Inti Administrasi Perpajakan.

Kementerian Energi dan Sumber Daya Mineral Republik Indonesia. (2025). Mineral and coal sector performance report 2025. Ministry of Energy and Mineral Resources.

Organisation for Economic Co-operation and Development. (2004). Compliance risk management: Managing and improving tax compliance. OECD. https://www.oecd.org/content/dam/oecd/en/topics/policy-issues/tax-administration/compliance-risk-management-managing-and-improving-tax-compliance.pdf

Organisation for Economic Co-operation and Development. (2023a). Revenue statistics in Asia and the Pacific 2023: Strengthening property taxation in Asia. OECD Publishing. https://doi.org/10.1787/e7ea496f-en

Organisation for Economic Co-operation and Development. (2023b). Tax administration 2023: Comparative information on OECD and other advanced and emerging economies. OECD Publishing. https://doi.org/10.1787/900b6382-en

Pemerintah Republik Indonesia. (1994). Undang-Undang Nomor 12 Tahun 1994 tentang Pajak Bumi dan Bangunan.

Pemerintah Republik Indonesia. (2025). Undang-Undang Nomor 2 Tahun 2025 tentang Perubahan Keempat atas Undang-Undang Nomor 4 Tahun 2009 tentang Pertambangan Mineral dan Batubara.

Sekaran, U., & Bougie, R. (2016). Research methods for business: A skill-building approach (7th ed.). John Wiley & Sons.

Sugiyono. (2013). Metode penelitian pendidikan: Pendekatan kuantitatif, kualitatif, dan R&D. Alfabeta.

United Nations Committee of Experts on Global Geospatial Information Management. (2020). Integrated geospatial information framework implementation guide. United Nations. https://ggim.un.org/IGIF/

van der Aalst, W. M. P. (2016). Process mining: Data science in action (2nd ed.). Springer. https://doi.org/10.1007/978-3-662-49851-4

World Bank. (2023). Property tax reform: Principles and international practices. World Bank.

World Bank. (2024). Digital government and domestic revenue mobilization. World Bank.