Effects of Tax Supervision and Socialization on Village Fund Tax Revenue Mediated by Taxpayer Compliance Level

Bilah Samping Artikel

Isi Artikel Utama

Abstrak

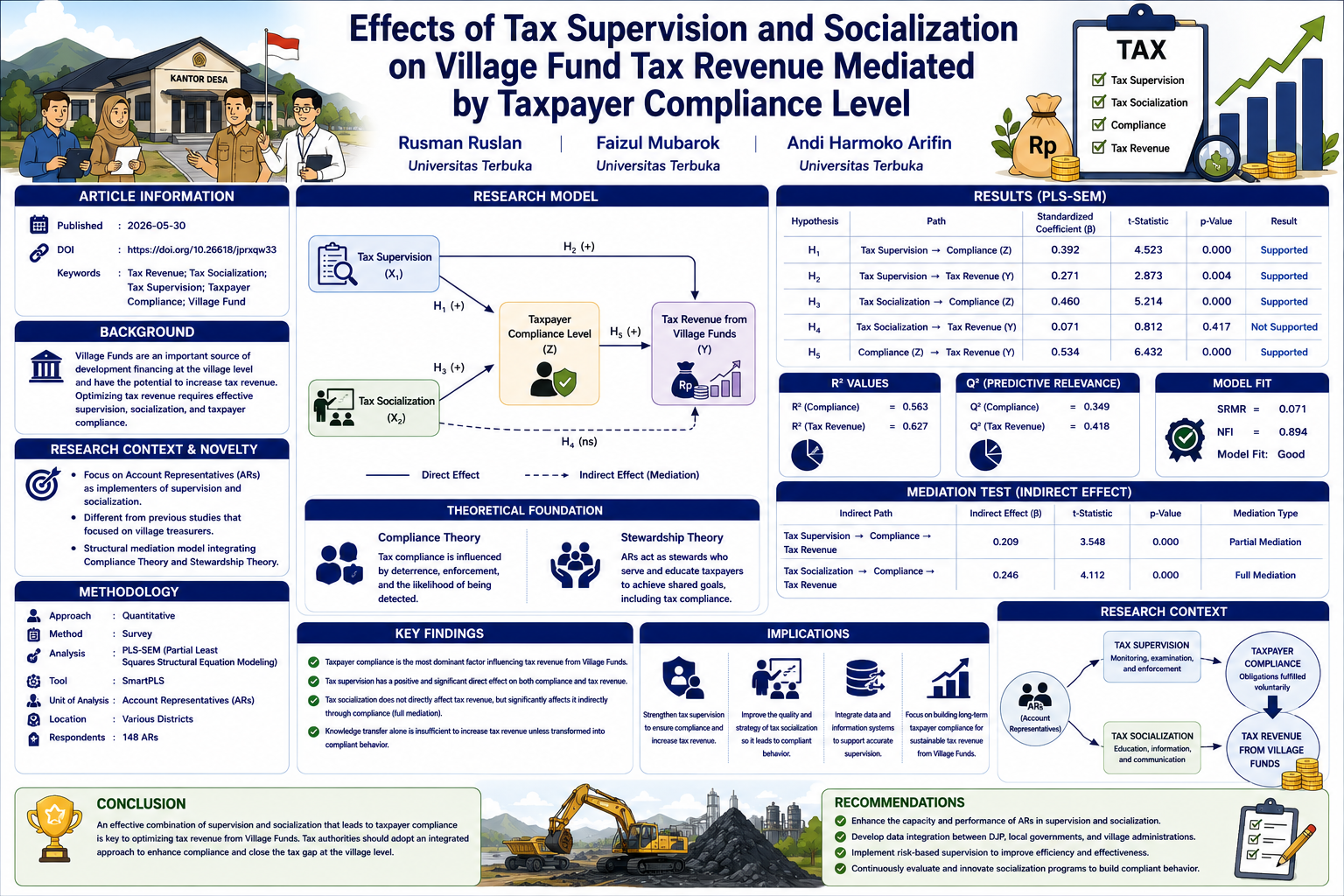

This study examines the effect of tax supervision and tax socialization on tax revenue from Village Funds, with taxpayer compliance serving as a mediating variable. The study is motivated by the importance of optimizing tax revenue at the village level and understanding the managerial and behavioral factors that influence taxpayer compliance. Unlike previous studies that mainly focused on village treasurers, this research emphasizes the perspective of Account Representatives (ARs) as the implementers of tax supervision and tax socialization. In addition, the study develops a structural mediation model integrating Compliance Theory and Stewardship Theory to explain the mechanisms through which tax supervision and tax socialization influence taxpayer compliance and tax revenue. A quantitative approach was employed using Partial Least Squares Structural Equation Modeling (PLS-SEM) to analyze both direct and indirect relationships among variables. The findings reveal that taxpayer compliance is the most dominant factor affecting tax revenue from Village Funds. Tax supervision has a positive and significant direct effect on both taxpayer compliance and tax revenue, indicating its important role in maintaining regulatory control and encouraging enforcement-based compliance. Meanwhile, tax socialization does not directly affect tax revenue but significantly influences it indirectly through taxpayer compliance, indicating a full mediation effect. These findings demonstrate that knowledge transfer alone is insufficient to increase tax revenue unless it is transformed into compliant behavior. Therefore, effective tax management requires a balanced integration of supervisory enforcement and educational approaches to foster sustainable taxpayer compliance and optimize tax revenue from Village Funds.

##plugins.themes.bootstrap3.displayStats.downloads##

Rincian Artikel

Terbitan

Bagian

Artikel ini berlisensi Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Referensi

Abada, M. F. I., & Winarsih. (2024). The Effect of E-Commerce, Tax, Supervision, and Tax Audit on Value-Added Tax Revenue (Case Study on Kudus Regency Taxpayers). Journal of Advanced Multidisciplinary Research, 5(1), 2723–6978. https://doi.org/10.30659/JAMR.4.2.13-27

Abdu, E., & Adem, M. (2023). Tax compliance behavior of taxpayers in Ethiopia: A review paper. In Cogent Economics and Finance (Vol. 11, Number 1). Cogent OA. https://doi.org/10.1080/23322039.2023.2189559

Andreas, & Savitri, E. (2015). The Effect of Tax Socialization, Tax Knowledge, Expediency of Tax ID Number and Service Quality on Taxpayers Compliance with Taxpayers Awareness as Mediating Variables. Procedia - Social and Behavioral Sciences, 211, 163–169. https://doi.org/10.1016/j.sbspro.2015.11.024

Betu, K. W., & Suninono, A. R. (2024). Analysis Of The Application Of Taxes To Village Fund Management. Jurnal Akuntansi Dan Bisnis Krisnadwipayana, 11, 2024. https://doi.org/10.35137/jabk.v11i2.406

BPS-Statistics Indonesia. (2024). Jumlah Desa/Kelurahan Menurut Provinsi, 2023.

Christian, F. F., & Aribowo, I. (2021). Pengawasan Kepatuhan Perpajakan Wajib Pajak Strategis Di KPP Pratama Sukoharjo (Supervision of Tax Compliance of Strategic Taxpayers at KPP Pratama Sukoharjo). Jurnal Pajak Indonesia, 5. www.jurnal.pknstan.ac.id/index.php/JPI

Damariyanti, A., & Fathah, R. N. (2023). Analisis Penerapan Perpajakan Dalam Pengelolaan Dana Desa (Analysis of Tax Implementation in Village Fund Management). Jurnal Ilmiah Multidisiplin, 2(8).

Defrizal, Wibowo, H. N. B., & Rizal, S. (2021). The Influence of Account Representative Supervision and the Implementation of Tax Sanctions on Compliance of Taxpayers in KPP Pratama Teluk Betung. International Journal of Research and Review, 8(2).

Devos, K. (2014). Factors Influencing Individual Taxpayer Compliance Behaviour. Springer.

Dharmawati, T., Yusuf, S., Mustari, W. O., & Fahmi, N. (2024). Pengaruh E-Commerce, Pengawasan Pajak dan Pemeriksaan Pajak Terhadap Penerimaan Pajak ( The Effect of E-Commerce, Tax Supervision, and Tax Audits on Tax Revenue). Jurnal Akuntansi Dan Keuangan, 09. http://jak.uho.ac.id/index.php/journal

Donaldson, L., & Davis, J. H. (1991). Stewardship Theory or Agency Theory: CEO Governance and Shareholder Returns. Australian Journal of Management 16.

Dularif, N., & Rustiarini, N. W. (2022). Tax compliance and non-deterrence approach: a systematic review. International Journal of Sociology and Social Policy, 42(11–12), 1080–1108.

Etzioni, A. (1961). A Comparative Analysis of Complex Organizations. https://www.jstor.org/stable/2091811?seq=1&cid=pdf-reference#references_tab_contents

Government of the Republic of Indonesia. (2021). Undang-Undang Republik Indonesia Nomor 7 Tahun 2021 tentang Harmonisasi Peraturan Perpajakan.

Government of the Republic of Indonesia. (2024). LKPP Tahun 2023 Audited (2023 Audited Central Government Financial Report).

Hair, J., Hult, G. T. M., Ringle, C., Sarstedt, M., Danks, N., & Ray, S. (2021). Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R: A workbook.

Hajawiyah, A., Suryarini, T., Kiswanto, & Tarmudji, T. (2021). Analysis of a tax amnesty’s effectiveness in Indonesia. Journal of International Accounting, Auditing and Taxation, 44. https://doi.org/10.1016/j.intaccaudtax.2021.100415

Handoko, Toni, N., & Simorangkir, E. N. (2021). Influence of Tax Socialization and Tax Knowlede on Tax Revenue with Taxpayer Compliance as A Moderating Variables at KPP Madya Medan. International Journal of Business, Economics and Law, 24.

Ministry of Finance of the Republic of Indonesia. (2021). Peraturan Menteri Keuangan Republik Indonesia Nomor 45/PMK.01/2021 tentang Account Representative pada Kantor Pelayanan Pajak. www.jdih.kemenkeu.go.id

Pijnenburg, M., Kowalczyk, W., & Dijk, L. V. D. H.-V. (2017). A Roadmap for Analytics in Taxpayer Supervision. In The Electronic Journal of e-Government (Vol. 15).

Rinaldi, A., & Devi, Y. (2021). Mathematical modeling for awareness, knowledge, and perception that influence willpower to pay tax using multiple regression. IOP Conference Series: Earth and Environmental Science, 1796(1). https://doi.org/10.1088/1742-6596/1796/1/012062

Rosdiana, H. (2021). Analysis of Tax Audit Policy Implementation in Indonesia View from the Principle of Equality between Taxpayer and Fiscus. Budapest International Research and Critics Institute (BIRCI-Journal): Humanities and Social Sciences, 4(4), 13391–13402.

Sarpong, S. A., Yeboah, M., Oware, K. M., & Danquah, B. A. (2024). Effect of Taxpayer Knowledge and Taxation Socialization on Taxpayer Compliance: The Mediating Role of Taxpayer Awareness. WSEAS Transactions On Business And Economics, 21, 1217–1227. https://doi.org/10.37394/23207.2024.21.99

Suharti, S., & Hidayatulloh, A. (2022). Sosialisasi Perpajakan, Pengetahuan Perpajakan, Kinerja Account Representative, Dan Kepatuhan Wajib Pajak Orang Pribadi (Tax Socialization, Tax Knowledge, Account Representative Performance, and Individual Taxpayer Compliance). Jurnal Aplikasi Akuntansi, 7(1), 1–11. https://doi.org/10.29303/jaa.v7i1.143

Yustina, A. I., & Hertiningtyas, I. (2021). Taxation Ethical Issues: Perspectives of Tax Professionals in Indonesia. The Indonesian Journal of Accounting Research, 24(01). https://doi.org/10.33312/ijar.503