Corporate Tax Avoidance in Emerging Markets: The Limited Role of ESG, Earnings Management, and Financial Leverage

Bilah Samping Artikel

Isi Artikel Utama

Abstrak

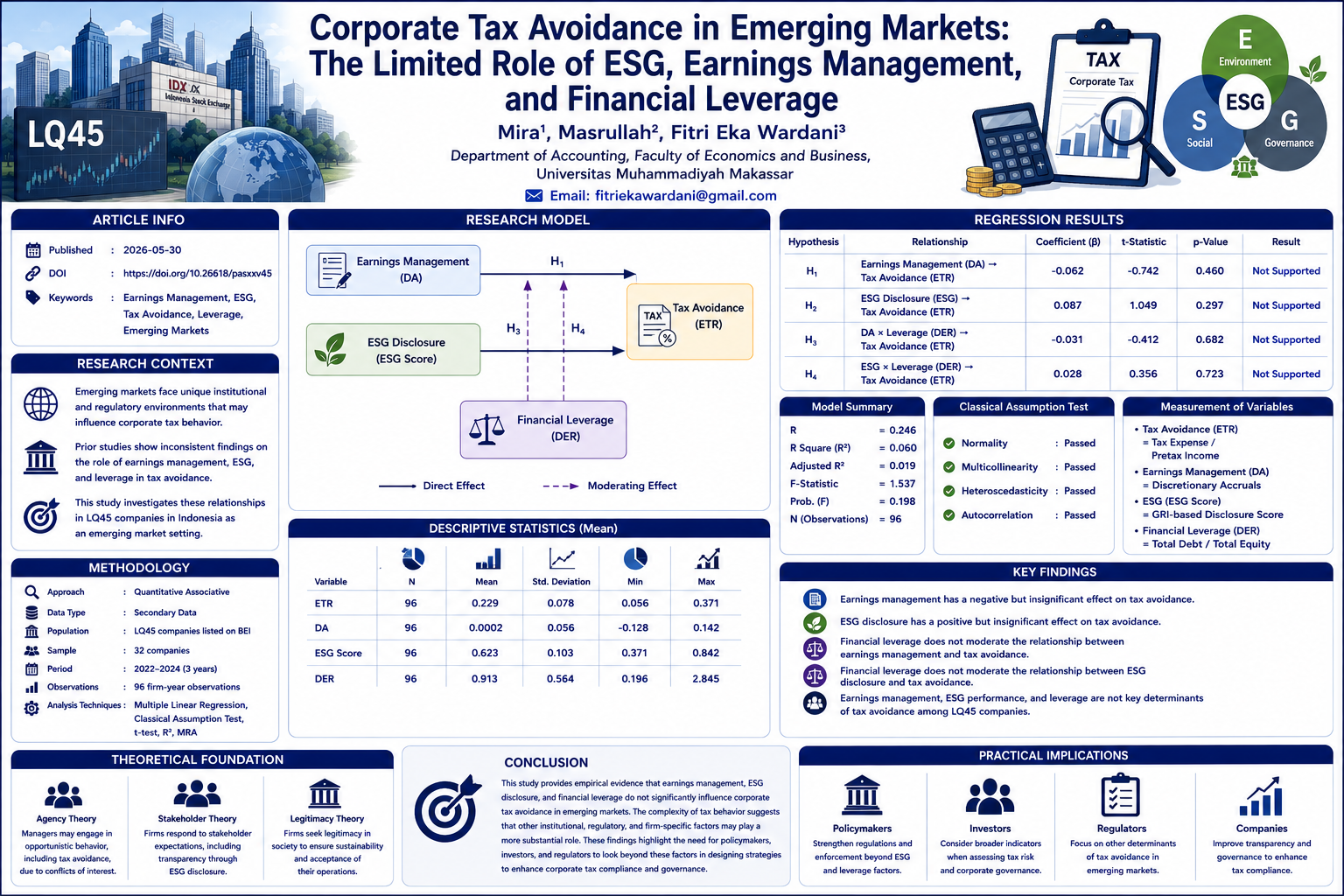

This study examines the effect of earnings management and Environmental, Social, and Governance (ESG) disclosure on corporate tax avoidance, with financial leverage as a moderating variable, in LQ45 companies listed on the Indonesia Stock Exchange. Grounded in agency, stakeholder, and legitimacy theories, this research aims to provide empirical evidence on the determinants of tax avoidance behavior in emerging markets. This study employs a quantitative associative approach using secondary data from 32 LQ45 companies over the 2022–2024 period, resulting in 96 firm-year observations. Tax avoidance is proxied by the Effective Tax Rate (ETR), earnings management by discretionary accruals (DA), ESG by disclosure scores based on Global Reporting Initiative (GRI), and leverage by the Debt-to-Equity Ratio (DER). Data analysis includes multiple linear regression, classical assumption tests, hypothesis testing (t-test), coefficient of determination (R²), and Moderated Regression Analysis (MRA). The results indicate that earnings management has a negative but insignificant effect on tax avoidance, while ESG disclosure shows a positive but insignificant relationship with tax avoidance. Furthermore, leverage is not found to moderate the relationship between earnings management and tax avoidance, nor between ESG and tax avoidance. These findings suggest that earnings management, ESG performance, and leverage are not key determinants of tax avoidance among LQ45 companies. The study highlights the complexity of corporate tax behavior and implies that other factors may play a more substantial role. The results provide important insights for policymakers, investors, and regulators in improving corporate tax compliance and governance practices in emerging markets.

##plugins.themes.bootstrap3.displayStats.downloads##

Rincian Artikel

Terbitan

Bagian

Artikel ini berlisensi Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Referensi

Agustini, Y., Azwardi, A., & Mukhtaruddin, M. (2023). The effect of environmental, social, and governance and financial distress on tax aggressiveness in Indonesia: CEO gender as a moderating variable. Jurnal Informatika Ekonomi Bisnis, 5, 920–926. https://doi.org/10.37034/infeb.v5i3.670

Amalia, R., & Kusuma, I. W. (2023). The effect of environmental, social, and governance performance on market performance with ESG controversy as a moderating variable. ABIS: Accounting and Business Information Systems Journal, 11(2). https://doi.org/10.22146/abis.v11i2.84771

Ambarwati, S., Azizah, W., & Aprizalni, L. (2024). Corporate governance and earnings management. Jurnal Akuntansi dan Bisnis Indonesia, 5(1), 73–84.

Aprilliana, D., Ajitama, O., Rachman, R. A., Wahono, P., & Pahala, I. (2024). The effect of firm performance on tax avoidance through firm size in LQ45 companies listed on IDX. Jurnal EBI, 6(1), 1–9. https://doi.org/10.52061/ebi.v6i1.229

Baroroh, F., & Kusumawati, E. (2024). The effect of institutional ownership, leverage, profitability, and media exposure on corporate social responsibility disclosure. Economics and Digital Business Review, 5(2), 678–692.

Christy, E., & Sofie. (2023). The effect of environmental, social, and governance disclosure. Jurnal Ekonomi Trisakti, 3(2), 3899–3908.

Divisi Perdagangan dan Riset. (2024). Evaluation of IDX30, LQ45, IDX80, KOMPAS100, PEFINDO25, BISNIS-27, MNC36, and SMinfra18 indices. Indonesia Stock Exchange.

Fajar, F. D. (2021). The effect of leverage, firm size, and profitability on accounting conservatism (Undergraduate thesis). Sekolah Tinggi Ilmu Ekonomi Indonesia Jakarta.

Falbo, T. D., & Firmansyah, A. (2021). Tax avoidance in Indonesia: Multinationality and earnings management. Bisnis-Net Jurnal Ekonomi dan Bisnis, 4(1), 94–110. https://doi.org/10.46576/bn.v4i1.1325

Ghazali, A., & Zulmaita. (2020). The effect of ESG disclosure on firm profitability: Evidence from infrastructure sector companies in Indonesia. Prosiding SNAM PNJ, 1–13.

Handayani, N. T., Marundha, A., & Khasanah, U. (2024). The effect of earnings management, profitability, and liquidity on tax avoidance. Jurnal Economina, 3(2), 197–218. https://doi.org/10.55681/economina.v3i2.1191

Harahap, N. D. (2020). Legal consequences for taxpayers committing tax crimes based on Indonesian tax law. Jurnal Ilmiah Maksitek, 5(3), 68.

Hasan, I., Lynch, D. K., & Siddique, A. R. (2022). Usefulness of hard information and soft information: Case of default risk and ESG factors. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4015878

Hidayat, H., & Wijaya, S. (2021). The effect of earnings management and transfer pricing on tax avoidance. Bina Ekonomi, 25(2), 155–173.

Imaniar, N. I., Rely, G., & Prayogo, B. (2024). The effect of capital intensity, leverage, and corporate social responsibility on tax management. SENTRI: Jurnal Riset Ilmiah, 3(2), 1099–1108. https://doi.org/10.55681/sentri.v3i2.2343

Lalita, A., & Rahayuningsih, D. A. (2024). The effect of corporate governance and firm characteristics on tax avoidance. Jurnal Ilmiah Akuntansi dan Keuangan, 3(1), 1–14. https://doi.org/10.24034/jiaku.v3i1.6245

Liana, L. (2009). Using MRA with SPSS to test moderating variables. Jurnal Teknologi Informasi Dinamik, 14(2), 90–97.

Manuel, D., Sandi, S., Firmansyah, A., & Trisnawati, E. (2022). Earnings management, leverage, and tax avoidance: The moderating role of CSR. Jurnal Pajak Indonesia, 6(2S), 550–560. https://doi.org/10.31092/jpi.v6i2s.1832

Maulana, A. (2022). Analysis of validity, reliability, and feasibility of instruments. Jurnal Kualita Pendidikan, 3(3), 133–139. https://doi.org/10.51651/jkp.v3i3.331

Muda, I., Abubakar, E., & others. (2020). The effect of firm size, profitability, leverage, and earnings management on tax avoidance moderated by political connection. Jurnal Riset Akuntansi dan Keuangan, 8(2), 375–392.

Nabiilah, A., & Fahira, H. (2024). The effect of corporate governance, internal auditor competence, and ESG on earnings management. Jurnal Ekonomi Manajemen dan Bisnis, 1(5), 77–87.

Pratiwi, N. I., Fuadah, L. L., & Yunisvita. (2024). The effect of ESG and capital intensity on tax avoidance. Management Studies and Entrepreneurship Journal, 5(2), 7772–7783.

Putri Heryana, R., Luthfi, D., & Santoso, R. A. (2024). The effect of profitability and leverage on tax avoidance. Jurnal Revenue: Jurnal Akuntansi, 5(1), 511–532.

Ruan, L., & Liu, H. (2021). ESG activities and firm performance: Evidence from China. Sustainability, 13(2), 1–16. https://doi.org/10.3390/su13020767

Sadjiarto, A., Alvin, J., Angela, L., & others. (2024). Earnings management and ESG on tax avoidance with leverage as moderating variable.

Sekar Sari, P., Widiatmoko, J., & others. (2023). ESG disclosure and financial performance with gender diversity as moderator. Jurnal Ilmiah Akuntansi dan Keuangan, 5(9), 3634–3642.

Setiawati, L., & Na’im, A. (2000). Earnings management. Jurnal Ekonomi dan Bisnis Indonesia, 15(4), 424–441.

Silvera, D. L., Heriyani, & Sahara. (2024). Corporate governance and CSR: Their impact on tax avoidance and earnings management. Jurnal Akademi Akuntansi Indonesia Padang, 4(1), 35–53. https://doi.org/10.31933/5dz3ke89

Syauqoti, R., & Ghozali, M. (2018). Analysis of Islamic and conventional financial institutions. Iqtishoduna, 15–30. https://doi.org/10.18860/iq.v0i0.4820

Triyani, A., Setyahuni, S. W., & Kiryanto, K. (2020). The effect of ESG disclosure on firm performance. Jurnal Reviu Akuntansi dan Keuangan, 10(2), 261–280. https://doi.org/10.22219/jrak.v10i2.11820

Utomo, P., Asvio, N., & Prayogi, F. (2024). Classroom action research methods. Pubmedia Jurnal Penelitian Tindakan Kelas Indonesia, 1(4), 19. https://doi.org/10.47134/ptk.v1i4.821

Wanda, A. P., & Halimatusadiah, E. (2021). The effect of solvency and profitability on tax avoidance. Jurnal Riset Akuntansi, 1(1), 59–65. https://doi.org/10.29313/jra.v1i1.194

Wijaya, S., & Hidayat, H. (2022). Earnings management and transfer pricing on tax avoidance. Bina Ekonomi, 25(2), 155–173. https://doi.org/10.26593/be.v25i2.5331

Yunita Ulandari, & Susila, G. P. A. J. (2024). The effect of ROA and DER on stock prices. Bisma: Jurnal Manajemen, 9(3), 363–369. https://doi.org/10.23887/bjm.v9i3.63826