The Influence of Tax Morale, Social Norms, and Trust in Government on Individual Taxpayer Compliance

Bilah Samping Artikel

Isi Artikel Utama

Abstrak

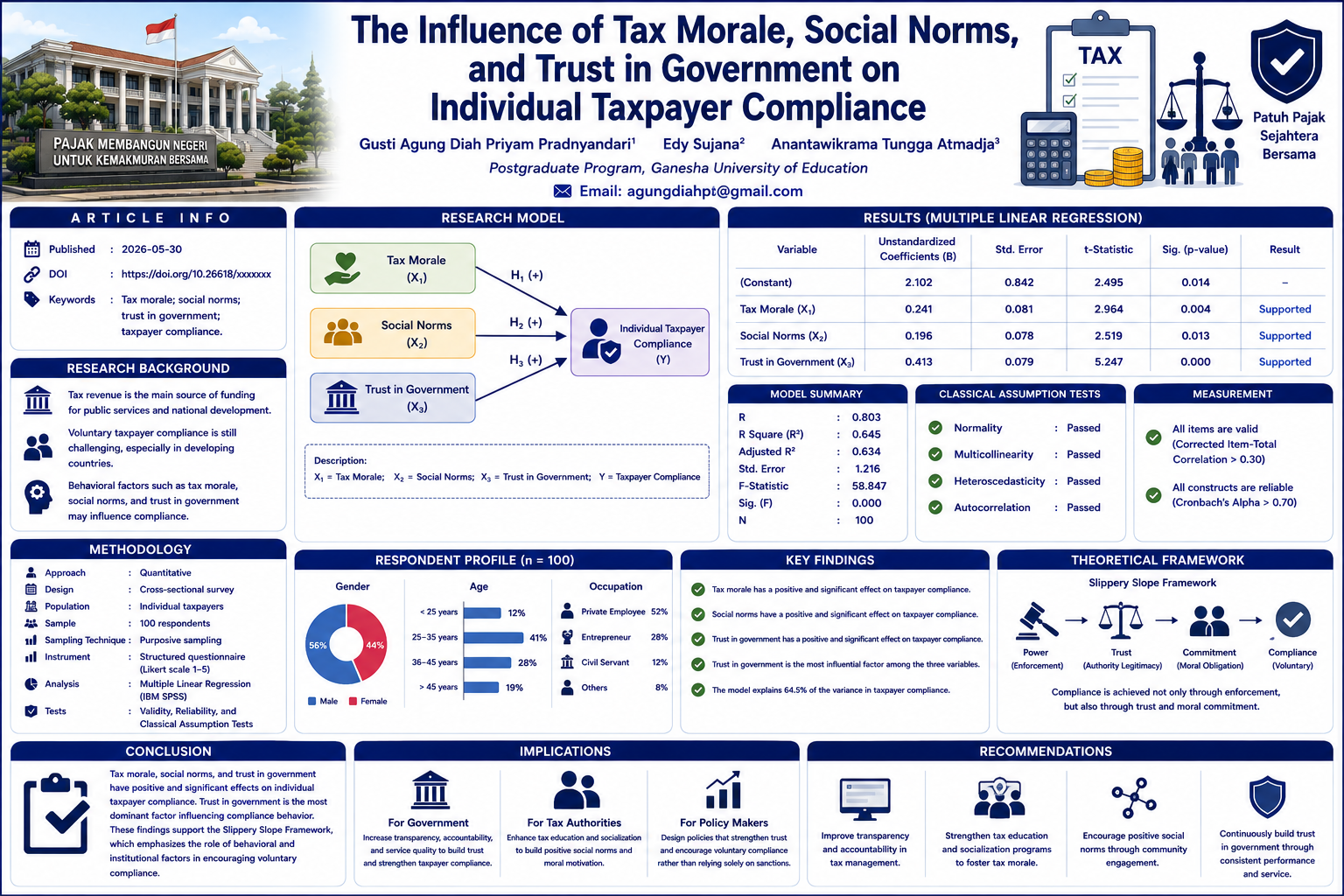

Taxpayer compliance remains a crucial issue in public finance because tax revenues constitute a primary source of government funding used to support public services and national development. However, maintaining voluntary taxpayer compliance continues to be a challenge, particularly in developing countries where behavioral factors may significantly influence taxpayers’ decisions. This study aims to examine the influence of tax morale, social norms, and trust in government on individual taxpayer compliance. The research employs a quantitative approach using a cross-sectional survey design. Primary data were collected from 100 individual taxpayers through a structured questionnaire distributed via an online survey. The data were analyzed using multiple linear regression with the assistance of IBM SPSS software. Prior to hypothesis testing, validity, reliability, and classical assumption tests were conducted to ensure the robustness of the regression model. The results indicate that tax morale, social norms, and trust in government have positive and statistically significant effects on taxpayer compliance. Among these variables, trust in government demonstrates the strongest influence on compliance behavior. These findings support the Slippery Slope Framework, which suggests that taxpayer compliance is shaped not only by enforcement mechanisms but also by behavioral and institutional factors. The study contributes to the literature on behavioral taxation by highlighting the importance of moral motivation, social influence, and institutional trust in encouraging voluntary taxpayer compliance.

##plugins.themes.bootstrap3.displayStats.downloads##

Rincian Artikel

Terbitan

Bagian

Artikel ini berlisensi Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Referensi

Alm, J., & Torgler, B. (2021). Do Ethics Matter? Tax Morale and Tax Compliance. Journal of Economic Behavior & Organization, 186, 545–566.

Bassey, E., Mulligan, E., & Ojo, A. (2022). A conceptual framework for digital tax administration - A systematic review. In Government Information Quarterly (Vol. 39, Number 4). Elsevier Ltd. https://doi.org/10.1016/j.giq.2022.101754

Bornman, M., & Ramutumbu, P. (2023). Tax Knowledge, Tax Morale and Tax Compliance Behavior Among Taxpayers. EJournal of Tax Research, 21(1), 1–20.

Darmayasa, I. N., & Hardika, N. S. (2024). Core tax administration system: the power and trust dimensions of slippery slope framework tax compliance model. Cogent Business and Management, 11(1). https://doi.org/10.1080/23311975.2024.2337358

Djafri, I. A., Damawati, I., Suharto, S., Satwika, I. G. A. R. P., & Rahmatullah, R. (2023). Utilization of Information and Communication Technology in the Tax Administration System to Increase Taxpayer Compliance. Ilomata International Journal of Tax and Accounting, 4(1), 14–25. https://doi.org/10.52728/ijtc.v4i1.670

Hidayatulloh, A., & Fikrianoor, K. (2023). Norma Pribadi dan Kepatuhan Wajib Pajak: Apakah Kepercayaan Pada Pemerintah Berperan? Jurnal Riset Akuntansi, 15(1), 24–33. https://doi.org/10.34010/jra.v15i1.8486

Jamel, M. F., & Cheisviyanny, C. (2024). Pengaruh Kepercayaan pada Pemerintah dan Persepsi Keadilan Pajak Terhadap Kepatuhan Pajak. JURNAL EKSPLORASI AKUNTANSI, 6(3), 913–931. https://doi.org/10.24036/jea.v6i3.1505

Mabrur, A., & Mohammad, C. H. N. (2025). Tax Compliance in The Digital Era: An Empirical Analysis of Perceived Justice, Trust, Tax Morale, and Knowledge Among The Younger Generation. Educoretax, 5(9), 1033–1048. https://doi.org/10.54957/educoretax.v5i9.1829

Maharani, F., Fionasari, D., & Putri, A. M. (2025). Pengaruh Kepercayaan Kepada Pemerintah, Keadilan Pajak, Dan Pendidikan PajakTerhadap Moral Pajak. Balance:Jurnal Akuntansi Dan Manajemen, 4.

Marfiana, A., Widyastuti, T., & Darmansyah, D. (2025). The Effect Of Social Norms And Perceived Justice Through Personal Norms And Government Trust On Voluntary Tax Compliance With Patriotism And Tax Morale As Moderating Variables.

Mpofu, F. Y. (2022). Green Taxes in Africa: Opportunities and Challenges for Environmental Protection, Sustainability, and the Attainment of Sustainable Development Goals. Sustainability (Switzerland), 14(16). https://doi.org/10.3390/su141610239

Novita, S., & Lasmana, M. S. (2024). Trust in Government and Tax Compliance in Indonesia and Malaysia: Do Ethics and Tax Amnesty Matter? International Journal of Economics and Financial Issues, 14(6), 31–48.

Nurhasan, Y., Sahara, L. I., Ramdani, C. S., & Septanta, R. (2025). Pengaruh Reformasi Perpajakan, Norma Subjektif dan Norma Sosial terhadap Kepatuhan Wajib Pajak. PRODUKTIF: Jurnal Kepegawaian Dan Organisasi, 4(1), 33–41. https://doi.org/10.37481/jko.v4i1.173

Oktafia, P. N., Hardiwinoto, H., Sinarasri, A., & Hanum, A. N. (2026). Analisis Pegaruh Kebijakan Pajak, Norma Subjektif dan Kinerja Keuangan terhadap Kepatuhan Pajak UMKM di Kota Semarang. Kompak :Jurnal Ilmiah Komputerisasi Akuntansi, 19(1), 01–11. https://doi.org/10.51903/kompak.v19i1.3212

Rahim, S., Rati, S., & Syahnur, K. N. F. (2023). Tax Morale dan Kepatuhan Pajak: Studi Empiris pada UMKM di Kota Makassar. Jurnal Ekonomi Bisnis, Manajemen Dan Akuntansi (JEBMA), 3(3), 863–874. https://doi.org/10.47709/jebma.v3i3.3136

Sari, M. I., & Fauzihardani, E. (2024). Pengaruh Kepercayaan Kepada Pemerintah, Norma Sosial, dan Sanksi Perpajakan terhadap Perilaku Kepatuhan Pajak. JURNAL EKSPLORASI AKUNTANSI, 6(1), 347–358. https://doi.org/10.24036/jea.v6i1.1046

Shelvi, & Rachmawati, T. (2025). Does Public Trust Encourage Voluntary Tax Compliance? A Study of Indonesian Taxpayers. Jurnal Ilmu Administrasi: Media Pengembangan Ilmu Dan Praktek Administrasi, 22(1), 31–48. https://doi.org/10.31113/jia.v22i1.1244

Subhan, S., Ustman, U., & Fahorrahman, F. (2023). Does Tax Morale Able to Moderate the Relationship Between Perceptions of Corruption and Taxpayer Compliance? Jurnal Akademi Akuntansi, 6(3), 385–399. https://doi.org/10.22219/jaa.v6i3.22895

Sugiyani, I. G. A. A., Yuesti, A., & Bhegawati, D. A. S. (2022). Pengaruh SosialisasiPajak, Pengetahuan Pajak, Kualitas Pelayanan, Sanksi Pajak, Kewajiban Moral Terhadap Kepatuhan Wajib PajakKendaraan Bermotor Di Kecamatan Mengwi Kabupaten Badung. JURNAL KARMA( Karya Riset Mahasiswa Akuntansi ), 2.

Wahyudin, D., Dwi Permana, R., & Ramadhan, M. I. (2025). Pengaruh Tax Morale, Kualitas Pelayanan, dan Kepercayaan pada Otoritas Pajak terhadap Kepatuhan Wajib di Pajak Kantor Pelayanan Pajak Pratama Kubu Raya. JUPASI), 44(1), 44–58. http://ojs.stiami.ac.id

Wibowo, J. Y., & Yanti, Y. (2024). The Effect of Tax Knowledge, Tax Sanctions, E-Filing on Tax Compliance. International Journal of Application on Economics and Business (IJAEB, 2(4), 2987–1972. https://doi.org/10.24912/ijaeb.v2i4.977

Wulandari, D. S., & Dasman, S. (2023). Taxpayer Compliance: The Role of Taxation Digitalization System and Technology Acceptance Model (TAM) with Internet Understanding as a Mediating Variable. East Asian Journal of Multidisciplinary Research, 2(6), 2385–2396. https://doi.org/10.55927/eajmr.v2i6.4653