Determinants of MSME Tax Compliance: Tax Knowledge, Tax Rates, and Digitalization

Bilah Samping Artikel

Isi Artikel Utama

Abstrak

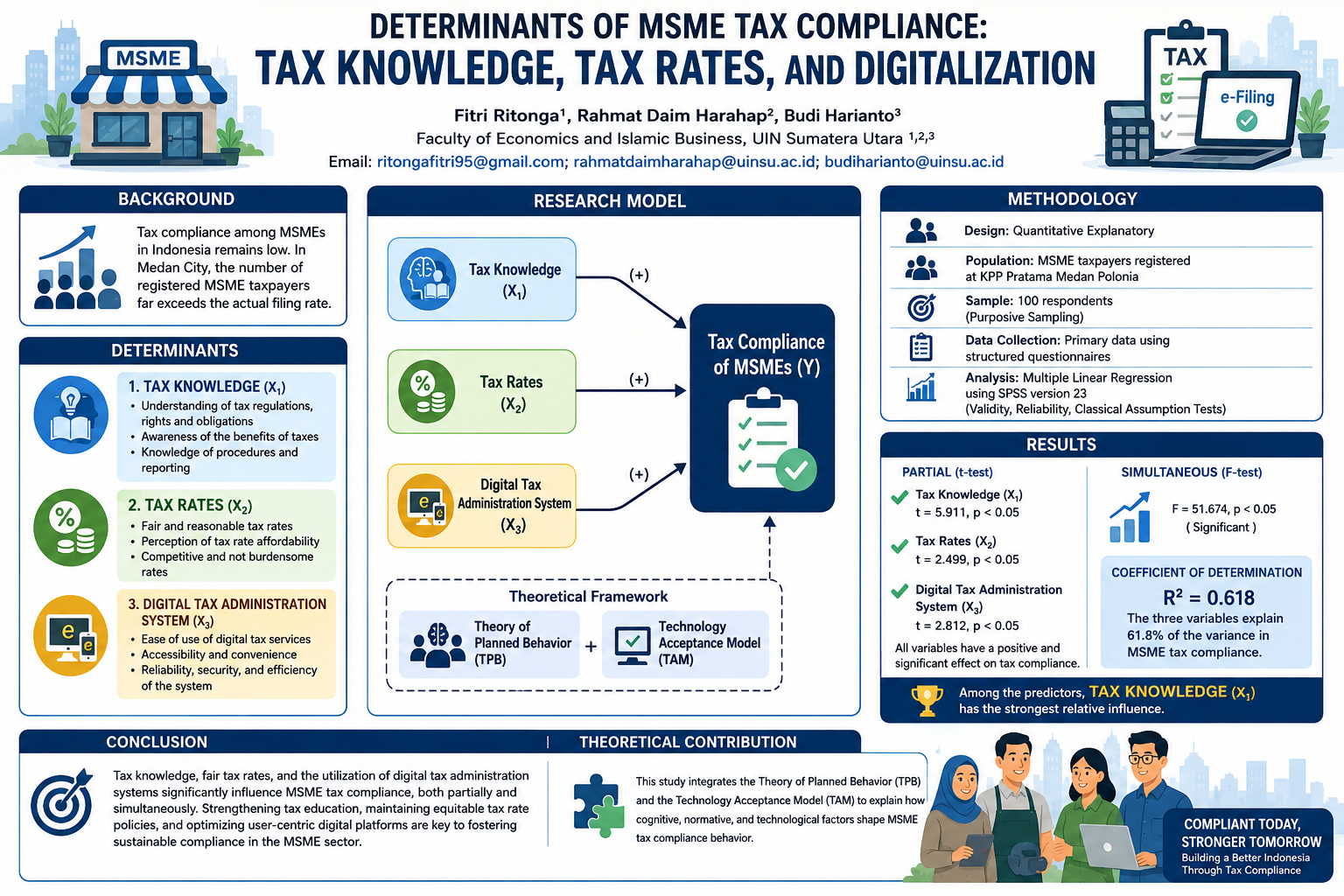

Tax compliance among Micro, Small, and Medium Enterprises (MSMEs) remains a persistent challenge in Indonesia, particularly in urban centers such as Medan City where registered taxpayer numbers far exceed actual filing rates. This study aims to analyze the influence of tax knowledge, tax rates, and the use of digital technology‑based tax administration systems on MSME tax compliance. A quantitative explanatory design was employed, utilizing primary data collected through structured questionnaires distributed to 100 MSME taxpayers registered at KPP Pratama Medan Polonia, selected via purposive sampling. Data analysis was conducted using multiple linear regression with SPSS version 23, preceded by validity, reliability, and classical assumption tests. The results reveal that partially, tax knowledge (t = 5.911, p < 0.05), tax rates (t = 2.499, p < 0.05), and the digital tax administration system (t = 2.812, p < 0.05) each exert a positive and significant effect on tax compliance. Simultaneously, the three variables significantly influence compliance (F = 51.674, p < 0.05), explaining 61.8% of its variance (R² = 0.618). Among the predictors, tax knowledge demonstrates the strongest relative influence. These findings underscore the importance of enhancing tax education, maintaining equitable rate policies, and optimizing user‑centric digital tax platforms to foster sustainable compliance within the MSME sector. The study contributes to the theoretical discourse by integrating the Theory of Planned Behavior and the Technology Acceptance Model within the tax compliance domain

##plugins.themes.bootstrap3.displayStats.downloads##

Rincian Artikel

Terbitan

Bagian

Artikel ini berlisensi Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Referensi

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/10.1016/0749-5978(91)90020-T

Ariyanto, D., Dewi, A. A., Paramadani, R. B., & Paramadina, A. A. (2024). Determinants of tax compliance and their impact on a sustainable information society: an investigation of MSMEs. Cogent Business & Management, 11(1), 1–19. https://doi.org/10.1080/23311975.2024.2414856

Dewi, S. K., Wibowo, M. R., Silalahi, A. D., & Irama, O. N. (2025). Pengaruh Literasi Pajak, Sistem Administrasi Pajak Digital, Sanksi Perpajakan Terhadap Kepatuhan Wajib Pajak UMKM Yang Terdaftar di KPP Pratama Medan Polonia. Worksheet: Jurnal Akuntansi, 5(1), 459–469. https://doi.org/10.46576/wjs.v5i1.7260

Dinda, A. N. S. (2020). Pengaruh Kesadaran Wajib Pajak, Kepercayaan Pada Pemerintah, dan Sanksi Pajak Terhadap Kepatuhan Wajib Pajak Usaha Mikro, Kecil, dan Menengah di Kecamatan Pakal (Studi Pada UMKM Yang Ada Di Area Pondok Benowo Indah). Universitas Wijaya Putra.

Hendrawati, E., Krivins, A., & Jaya, I. M. L. M. (2025). Tax Compliance Behavior of E-Commerce MSMEs in Surabaya : Evidence from the E-Peken Platform. International Journal of Social Science and Business, 9(3), 555–563. https://doi.org/10.23887/ijssb.v9i3.95263

Jamel, M. F., & Cheisviyanny, C. (2024). Pengaruh Kepercayaan pada Pemerintah dan Persepsi Keadilan Pajak Terhadap Kepatuhan Pajak. Jurnal Eksplorasi Akuntansi (JEA), 6(3), 913–931. https://doi.org/10.24036/jea.v6i3.1505

Khan, M. A., & Tjaraka, H. (2024). Tax justice and understanding: MSME compliance with Tax Regulation No. 55/2022 in Surabaya, Indonesia. Cogent Business & Management, 11(1), 1–19. https://doi.org/10.1080/23311975.2024.2396042

Kristiana, D. R., Kristianti, I. P., & Setyaningsih, P. R. A. (2025). The Role Of Digital Transactions, Tax Policy, And Ctas In Shaping Taxpayer Compliance: A Case Study Of Indonesian SMES. International Journal of Business and Society, 26(3), 825–841. https://doi.org/10.33736/ijbs.7925.2025

Listya, T., & Limajatini. (2022). Pengaruh Pengetahuan Pajak,Sosialisasi Pajak, dan Insentif Pajak Terhadap Kepatuhan Wajib Pajak Penggiat UMKM di Kecamatan Periuk. Prosiding Ekonomi Dan Bisnis. https://jurnal.buddhidharma.ac.id/index.php/pros/article/view/1402

Mahindra, M. I. (2020). PENGARUH PERUBAHAN TARIF, SANKSI DAN KESADARAN PERPAJAKAN TERHADAP KEPATUHAN WAJIB PAJAK UMKM [UNIVERSITAS ISLAM INDONESIA]. https://dspace.uii.ac.id/bitstream/handle/123456789/28473/16312165 Maulana Istar Mahindra.pdf?sequence=1

Marliyah, Nawawi, Z. M., & Humairoh, J. (2022). Strategi Peningkatan Ekonomi dan Tinjauan Ekonomi Islam Masa Covid 19 (Studi Kasus: UMKM di Kota Medan). Jurnal Ilmiah Ekonomi Islam, 8(2), 2027–2035. https://doi.org/10.29040/jiei.v8i2.5798

Michael, & Widjaja, W. (2024). DYNAMICS OF TAX EVASION IN INDONESIAN SMES: TAX RATES, SELF- ASSESSMENT SYSTEMS, AND TAX MORALE. Soedirman Accounting Review (SAR): Journal of Accounting and Business, 01(02), 32–46. https://doi.org/10.32424/1.sar.2024.9.01.11665

Nastiti, P. K. Y., Damayanti, T. W., Rita, M. R., & Supramono. (2025). Role of business sustainability, patriotism of business actors, and digital transformation in increasing MSME tax compliance. Cogent Business & Management, 12(1), 1–17. https://doi.org/10.1080/23311975.2025.2459328

Nurafiza, B., Kisnawati, B., & Rusdi. (2024). Analisis Pengaruh Digital Teknologi, Pengetahuan Pajak, Dan Sosialisasi Perpajakan Terhadap Kepatuhan Wajib Pajak. Akuntabel: Jurnal Ilmiah Akuntansi, 2(1), 49–61. https://journal.stieamm.ac.id/akuntabel/article/view/395

Peraturan Pemerintah (PP) Nomor 23 Tahun 2018 Tentang Pajak Penghasilan Atas Penghasilan Dari Usaha Yang Diterima Atau Diperoleh Wajib Pajak Yang Memiliki Peredaran Bruto Tertentu, Pub. L. No. 23 (2018).

Rahayu, S. K. (2017). Perpajakan Indonesia : Konsep dan Aspek Formal. Graha Ilmu.

Saputra, H. (2019). ANALISA KEPATUHAN PAJAK DENGAN PENDEKATAN TEORI PERILAKU TERENCANA (THEORY OF PLANNED BEHAVIOR) (TERHADAP WAJIB PAJAK ORANG PRIBADI DI PROVINSI DKI JAKARTA). Jurnal Muara Ilmu Ekonomi Dan Bisnis, 3(1), 47–58. https://doi.org/10.24912/jmieb.v3i1.2320

Saputri, S. S. K., Yani, A., Suaidah, I., & Srikalimah. (2025). Pengaruh Pengetahuan Pajak, Sanksi Pajak, dan Digitalisasi Pajak terhadap Kepatuhan Wajib Pajak dengan Kemampuan Membayar Pajak sebagai Variabel Moderasi (Studi Kasus pada UMKM di Kabupaten Kediri). RIGGS: Journal of Artificial Intelligence and Digital Business, 4(3), 7808–7820. https://doi.org/10.31004/riggs.v4i3.3105

Saragih, F., Harahap, R. D., & Nurlaila. (2023). Perkembangan UMKM Di Indonesia: Peran Pemahaman Akuntansi, Teknologi Informasi dan. Owner: Riset & Jurnal Akuntansi, 7(3), 2518–2527. https://doi.org/10.33395/owner.v7i3.1427

Sitepu, W. R. B., & Arbak, S. (2023). Factors Affecting Tax Compliance by Small and Medium Enterprises in Indonesia. Oblik i Finansi, 4(102), 60–71. https://doi.org/10.33146/2307-9878-2023-4(102)-60-71

Subarkah, J., & Dewi, M. W. (2017). PENGARUH PEMAHAMAN, KESADARAN, KUALITAS PELAYANAN, DAN KETEGASAN SANKSI TERHADAP KEPATUHAN WAJIB PAJAK ORANG PRIBADI DI KPP PRATAMA SUKOHARJO. Jurnal Akuntansi Dan Pajak, 17(2). https://jurnal.stie-aas.ac.id/index.php/jap/article/view/210

Teguh, G., Muttiwijaya, P., Padang, R. R., Yasa, I. N. P., & Adiputra, I. M. P. (2025). Digital Transformation in Tax Administration : The Role of Coretax , Service Quality , and Morality in Enhancing MSME Compliance in Indonesia. The Indonesian Journal of Accounting Researchdo, 28(2), 359–410. https://doi.org/10.33312/ijar.947

Tsabita, P., Pebriani, R. A., & Meiriasari, V. (2025). Pengaruh Pemahaman Peraturan Perpajakan dan Tarif Pajak Terhadap Kepatuhan Wajib Pajak dengan Account Representative (AR) sebagai Variabel Moderasi di KPP Ilir Timur. Journal of Accounting and Finance Management, 6(1), 141–157. https://doi.org/10.38035/jafm.v6i1.1607

Undang-Undang Nomor 16 Tahun 2009 Tentang Penetapan Peraturan Pemerintah Pengganti Undang-Undang Nomor 5 Tahun 2008 Tentang Perubahan Keempat Atas Undang-Undang Nomor 6 Tahun 1983 Tentang Ketentuan Umum Dan Tata Cara Perpajakan Menjadi Undang-Undang, Pub. L. No. 16 (2009). https://peraturan.bpk.go.id/details/38624/uu-no-16-tahun-2009

Wardani, D. K., & Rumiyatun. (2017). PENGARUH PENGETAHUAN WAJIB PAJAK, KESADARAN WAJIB PAJAK, SANKSI PAJAK KENDARAAN BERMOTOR, DAN SISTEM SAMSAT DRIVE THRU TERHADAP KEPATUHAN WAJIB PAJAK KENDARAAN BERMOTOR. Jurnal Akuntansi, 5(1), 15–24. https://doi.org/10.24964/ja.v5i1.25324.

Yuliana, Asmapane, S., & Lahjie, A. A. (2022). Pengaruh Persepsi Kebermanfaatan, Kemudahan Penggunaan, Dan Kepuasan Wajib Pajak Terhadap Penggunaan e-Filing Bagi Wajib Pajak Di Samarinda. Jurnal Ilmu Akuntansi Mulawarman, 7(2). https://doi.org/10.30872/jiam.v8i1.10582