Determinants of Taxpayer Compliance in the Implementation of the Coretax System

Bilah Samping Artikel

Isi Artikel Utama

Abstrak

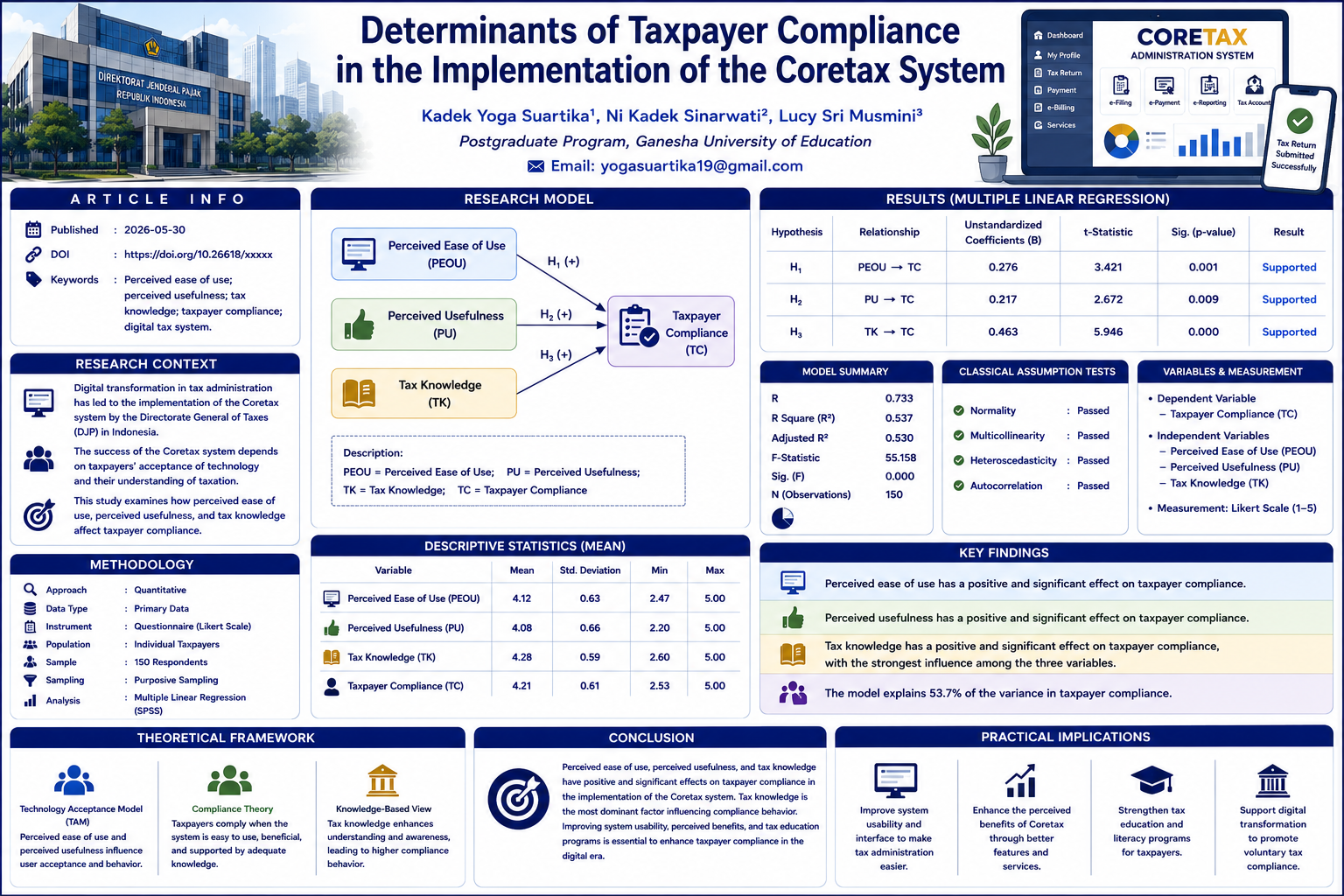

Taxpayer compliance is a fundamental factor in ensuring sustainable government revenue, particularly in the era of digital tax administration. The rapid development of information technology has encouraged tax authorities to modernize administrative systems to improve efficiency, transparency, and service quality. In Indonesia, the Directorate General of Taxes has implemented the Core Tax Administration System (Coretax) as an integrated digital platform designed to simplify tax administration processes. However, the effectiveness of this system largely depends on taxpayers’ acceptance of technology and their understanding of taxation. Therefore, this study aims to examine the effect of perceived ease of use, perceived usefulness, and tax knowledge on taxpayer compliance in the implementation of the Coretax system. This study employed a quantitative research approach using primary data collected through questionnaires distributed to 150 individual taxpayers selected using purposive sampling. The data were analyzed using multiple linear regression analysis with the assistance of SPSS software. The results indicate that perceived ease of use, perceived usefulness, and tax knowledge have positive and significant effects on taxpayer compliance. Among these variables, tax knowledge demonstrates the strongest influence on compliance behavior. These findings suggest that taxpayer compliance in the digital era is influenced not only by technological aspects but also by taxpayers’ understanding of tax regulations and procedures. This study contributes to the development of the Technology Acceptance Model in the context of digital tax administration and provides practical implications for tax authorities in improving system usability, perceived benefits, and tax education programs to enhance taxpayer compliance.

##plugins.themes.bootstrap3.displayStats.downloads##

Rincian Artikel

Terbitan

Bagian

Artikel ini berlisensi Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Referensi

Abu-Silake, S. A., Alshurafat, H., Alaqrabawi, M., & Shehadeh, M. (2024). Exploring the key factors influencing the actual usage of digital tax platforms. Discover Sustainability, 5(1), 88. https://doi.org/10.1007/s43621-024-00241-2

Abuur, E. S. (2022). Persepsi Kemudahan Dan Persepsi Kegunaan Terhadap Kepatuhan Wajib Pajak Dimediasi Oleh Penggunaan E-Filing. Jurnal Akuntansi Dan Keuangan Daerah, 17, 168–177.

Aini, A. N. (2025). Pengaruh Literasi Pajak, Digitalisasi Pajak Dan Sosialisasi Pajak Terhadap Kepatuhan Wajib Pajak. Prosiding Nasional Penelitian & Pengabdian Kepada Masyarakat, 2.

Al-Okaily, M. (2024). Advancements and forecasts of digital taxation information systems usage and its impact on tax compliance: does trust and awareness make difference? Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-09-2023-0567

Anggraeni, W. A. (2025). E-Taxation and Fiscal Governance: A Narrative Review of Compliance, Efficiency, and Equity. Summa : Journal of Accounting and Tax, 3(2), 97–110. https://doi.org/10.61978/summa.v3i2.970

Azzahra, N., & Sofianty, D. (2023). Pengaruh Kesadaran Wajib Pajak dan Pengetahuan Pajak terhadap Kepatuhan Wajib Pajak Orang Pribadi. Bandung Conference Series: Accountancy, 3(1). https://doi.org/10.29313/bcsa.v3i1.5853

Bassey, E., Mulligan, E., & Ojo, A. (2022). A conceptual framework for digital tax administration - A systematic review. In Government Information Quarterly (Vol. 39, Number 4). Elsevier Ltd. https://doi.org/10.1016/j.giq.2022.101754

Bellon, M., Dabla-Norris, E., Khalid, S., Carlos Paliza, J., Chang, J., & Villena, P. (2022). Digitalization and Tax Compliance Spillovers: Evidence from a VAT e-Invoicing Reform in Peru, WP/22/57, March 2022.

Darmayasa, I. N., & Hardika, N. S. (2024). Core tax administration system: the power and trust dimensions of slippery slope framework tax compliance model. Cogent Business and Management, 11(1). https://doi.org/10.1080/23311975.2024.2337358

Darono, A., & Panggabean, T. (2026). From Compliance to Adoption: A Theory-Building Study of Technology Implementation Gaps in Tax Administration. Journal of Risk and Financial Management, 19(4), 237. https://doi.org/10.3390/jrfm19040237

Ditha, A., Pratiwi, S., Erna, K., & Sinaga2, C. (2023). Pengaruh Motivasi, Pengetahuan Perpajakan, dan Sanksi Pajak Terhadap Kepatuhan Pajak (Vol. 15).

Djafri, I. A., Damawati, I., Suharto, S., Satwika, I. G. A. R. P., & Rahmatullah, R. (2023). Utilization of Information and Communication Technology in the Tax Administration System to Increase Taxpayer Compliance. Ilomata International Journal of Tax and Accounting, 4(1), 14–25. https://doi.org/10.52728/ijtc.v4i1.670

Habibah, M., Kusuma, I. C., & Jamaludin Aziz, A. (2026). The Effect of Taxpayer Awareness, Socialization, Sanctions and Accountability on Motor Vehicle Taxpayer Compliance. Jurnal Ilmiah Akuntansi Kesatuan, 12(6), 377–388. https://doi.org/10.37641/jiakes.v12i6.1612

Hanik, R. (2022). Pengaruh Persepsi Kemudahan, Persepsi Keadilan, Dan Sosialisasi Pajak Terhadap Kepatuhan Wajib Pajak Umkm Pada Masa Covid 19. Jurnal Ilmiah Mahasiswa FEB, 10.

Hikmah, Ratnawati, A. T., & Darmanto, S. (2023). Role of Attitude and Intention on the Relationship between Perceived Ease of Use, Perceived Usefulness, Trust, and E-Tax System Behavior. GLOBAL BUSINESS FINANCE REVIEW, 28(7), 89–104. https://doi.org/10.17549/gbfr.2023.28.7.89

Iramaidha, A. E., Hidayat, K., Fahrudi, A. N. L. I., & Nurrohman, R. (2025). Assessing the Impact of Service Quality, Perceived Usefulness, and Ease of Use on E-Filing Adoption: A Technology Acceptance Model (TAM) Perspective on Taxpayer Satisfaction and Compliance. International Journal of Research and Innovation in Social Science, IX(XIV), 610–618. https://doi.org/10.47772/IJRISS.2025.914MG0047

Mangoting, Y., Widuri, R., Dogi, D. C. P., & Gabronino, R. (2024). Exploring the Potential of Blockchain Technology in Digital Tax Administration to Enhance Tax Compliance. Jurnal Akuntansi Dan Keuangan, 26(2), 77–90. https://doi.org/10.9744/jak.26.2.77-90

Nasiroh, D., & Afiqoh, N. W. (2023). Pengaruh Pengetahuan Perpajakan, Kesadaran Perpajakan, Dan Sanksi Perpajakan Terhadap Kepatuhan Wajib Pajak Orang Pribadi. RISTANSI: Riset Akuntansi, 3(2), 152–164. https://doi.org/10.32815/ristansi.v3i2.1232

Ramadhan, G., & Wijaya, S. (2025). Implementasi Core Tax Administration System (Coretax) dalam pelaporan pajak: Analisis Technology Acceptance Model di PT ABC. Akuntansiku, 4(4), 303–315. https://doi.org/10.54957/akuntansiku.v4i4.1644

Rizkina, M. (2025). Reinventing Central Tax Administration: a Systematic Literature Review on Digital Tax Transformation and Compliance Enhancement in 2020–2025. Action Research Literate, 9(12). https://doi.org/10.46799/arl.v9i12.3072

Supriyati, S., Oktarina, D., Rokhmania, N., & Prananjaya, K. P. (2025). Tax Digitalization and Justice with Taxpayer Compliance and the Mediating Role of Tax Awareness. Aptisi Transactions on Technopreneurship (ATT), 7(2). https://doi.org/10.34306/att.v7i2.512

Tri Diyah Agustin, N. (2023). Pengaruh Pengetahuan Perpajakan, Persepsi Kemudahan, Keamanan dan Kerahasiaan Penggunaan E-Filing Terhadap Kepatuhan Wajib Pajak.

Venkatesh, V., Thong, J. Y. L., & Xu, X. (2016). Unified theory of acceptance and use of technology: A synthesis and the road ahead. Journal of the Association for Information Systems, 17(5), 328–376. https://doi.org/10.17705/1jais.00428

Wulandari, D. S., & Dasman, S. (2023). Taxpayer Compliance: The Role of Taxation Digitalization System and Technology Acceptance Model (TAM) with Internet Understanding as a Mediating Variable. East Asian Journal of Multidisciplinary Research, 2(6), 2385–2396. https://doi.org/10.55927/eajmr.v2i6.4653

Wulandari, W., Djaddang, S., & Suratno, S. (2025). Digital Era Tax Compliance: A Systematic Review Integrating Behavioral, Technological, and Institutional Perspectives. International Journal of Current Science Research and Review, 08(12). https://doi.org/10.47191/ijcsrr/V8-i12-58