What Drives Corporate Tax Avoidance in Indonesia’s Basic Materials Sector?

Bilah Samping Artikel

Isi Artikel Utama

Abstrak

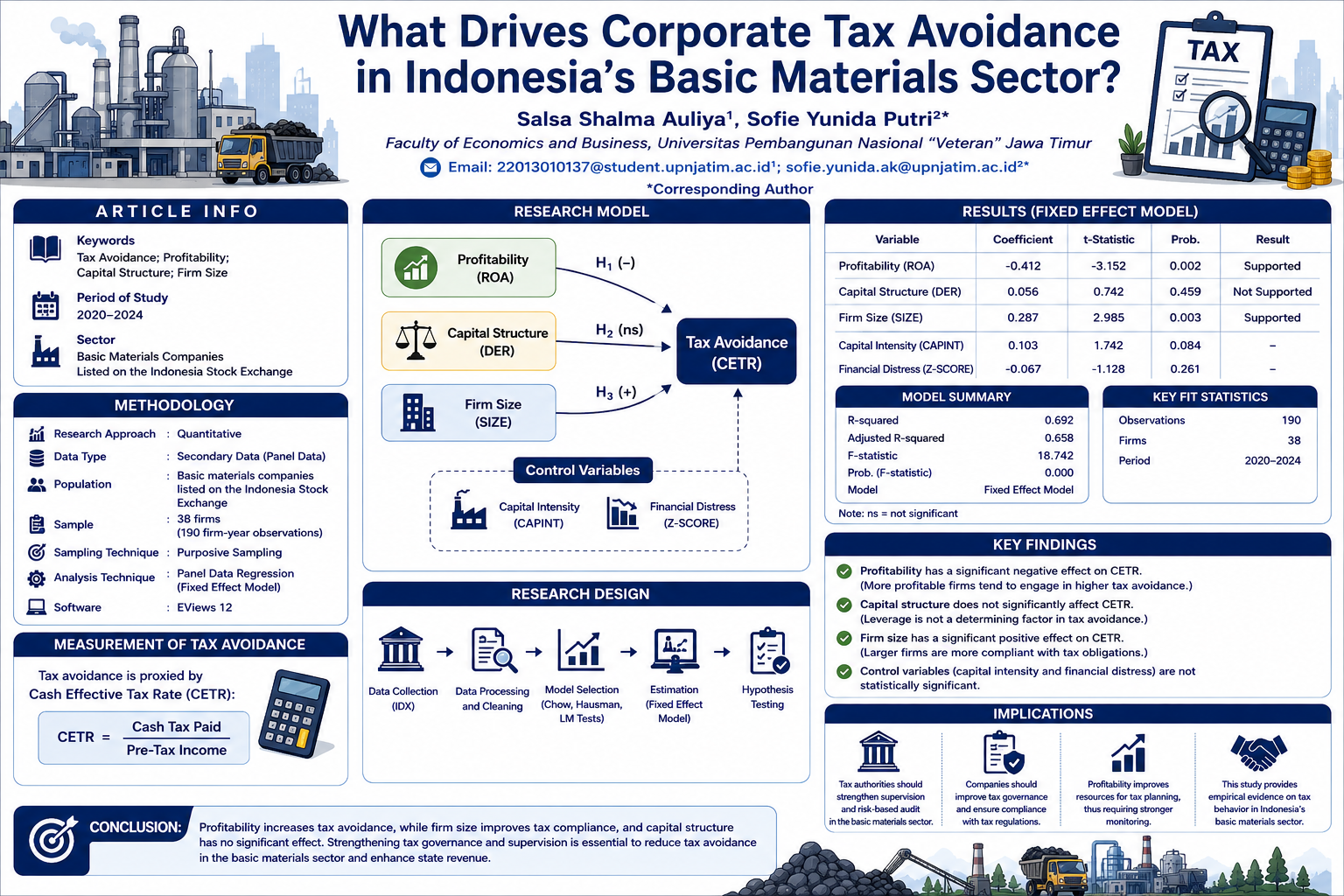

This study's goal is to examine how tax avoidance tactics, as calculated by the Cash Effective Tax Rate (CETR), are affected by profitability (ROA), capital structure (DER), and firm size (SIZE). This research employs a quantitative methodology and focuses on firms in the basic materials industry that are listed on the Indonesia Stock Exchange (IDX) between 2020-2024. Purposive sampling was utilized to choose the sample, which included 38 businesses with 190 observational data points. Panel data regression was used for analyzing data and the Fixed Effect Model (FEM) was chosen to serve as the model, incorporating capital intensity and financial distress as control variables. The results indicate that profitability has a significant negative effect on CETR. Capital structure does not affect CETR, while firm size has a significant positive effect on CETR. These findings are expected to provide practical implications for policymakers in formulating tax supervision regulations, as well as serve as a consideration for companies in managing corporate tax governance.

##plugins.themes.bootstrap3.displayStats.downloads##

Rincian Artikel

Terbitan

Bagian

Artikel ini berlisensi Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Referensi

Adiguna, S., & Ritonga, F. (2024). The Effect of Transfer Pricing and Profitability on Tax Avoidance Empirical Study in Industrial Sector Companies. Jurnal Ilmiah Akuntansi Kesatuan, 12(3), 421–430. https://doi.org/10.37641/jiakes.v12i3/2718

Arianti, B. F., & Soesila, B. (2025). Analysis of Capital Stucture, Leverage, and Sales Growth in Term of Tax Avoidance. Journal of Accounting and Business Education, 9(4), 19–31. https://doi.org/10.17977/jabe.v9i4.62218

Asqolani, Adhitama, S., & Johantri, B. (2024). Era Baru Program Relawan Pajak: Pemanfaatan Media Sosial Dalam Penyuluhan Pajak. Jurnal Keuangan Umum Dan Akuntansi Terapan (KUAT), 6(2), 100.

Cuevas-Vargas, H., Cortés-Palacios, H. A., & Lozano-García, J. J. (2021). Impact of capital structure and innovation on firm performance. Direct and indirect effects of capital structure. Procedia Computer Science, 199. https://doi.org/10.1016/j.procs.2022.01.137

Darma, S. S., & Amelia, K. Z. (2025). Pengaruh Struktur Modal, Beban Pajak Tangguhan dan Pertumbuhan Penjualan terhadap Penghindaran Pajak. SCIENTIFIC JOURNAL OF REFLECTION : Economic, Accounting, Management and Business, 8(4), 1496–1505.

Dewi, N. P. S. S., & Putri, I. G. A. M. A. D. (2021). Corporate Social Responsibility dan Free Cash Flow pada Tax Avoidance. E-Jurnal Akuntansi, 31(5). https://doi.org/10.24843/eja.2021.v31.i05.p01

Efendi, M., & Winingrum, S. P. (2025). Pengaruh Struktur Modal, Capital Intensity, Dan Ukuran Perusahaan Terhadap Tax Avoidance. Jurnal Ekonomika Dan Bisnis (JEBS), 5(1), 269–280. https://doi.org/10.47233/jebs.v5i1.2496

Gumelar, A., Susanto, H., & Sukayat, H. (2024). Effect Of Profitability, Leverage, Firm Size On Tax Avoidance Case study on Banking Companies Listed on the IDX 2023 Period. Jurnal Ilmiah Akuntansi Kesatuan, 12(3), 341–350. https://doi.org/10.37641/jiakes.v12i2.1435

Hardana, A., & Hasibuan, A. N. (2023). The Impact of Probability, Transfer Pricing, and Capital Intensity on Tax Avoidance When Listed Companies in the Property and Real Estate Sub Sectors on the Indonesia Stock Exchange. International Journal of Islamic Economics, 5(01). https://doi.org/10.32332/ijie.v5i01.6991

Haztania, S., & Lestari, T. U. (2023). Pengaruh Transfer Pricing, Karakter Eksekutif, dan Koneksi Politik Terhadap Tax Avoidance. Cakrawala Repositori IMWI, 6(1). https://doi.org/10.52851/cakrawala.v6i1.112

Hossain, M. S., Ali, M. S., Islam, M. Z., Ling, C. C., & Fung, C. Y. (2024). Nexus between profitability, firm size and leverage and tax avoidance: evidence from an emerging economy. Asian Review of Accounting, 32(5). https://doi.org/10.1108/ARA-08-2023-0238

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4). https://doi.org/10.1016/0304-405X(76)90026-X

Kalbuana, N., Taqi, M., Uzliawati, L., & Ramdhani, D. (2023). CEO Narcissism, Corporate Governance, Financial Distress, and Company Size on Corporate Tax Avoidance. Cogent Business and Management, 10(1). https://doi.org/10.1080/23311975.2023.2167550

Keryn, T., Lubis, S., & Mikroskil, U. (2025). Analysis Of Factors That Influence Tax Avoidance With Company Size As An Intervening Variable In Consumer Companies On The Indonesian Stock Exchange Period 2021-2023. Management Studies and Entrepreneurship Journal, 6(4), 5721–5744. http://journal.yrpipku.com/index.php/msej

Ma’sum, M. A., Jaeni, & Badjuri, A. (2023). Tax Avoidance dalam Perspektif Agency Theory (Studi Empiris Pada Karakteristik Teks Laporan Tahunan). Jurnal Ilmiah MEA (Manajemen, Ekonomi, Dan Akuntansi), 7(2), 1873–1884. https://doi.org/10.31955/mea.v7i2.3349

Ministry of Finance. (2024). APBN KiTa Desember 2024. APBN KiTA. https://www.kemenkeu.go.id/apbnkita

Ningrum, N. A., Herawati, R., Isthika, W., & Setyowati, L. (2025). Determinan Financial Distress, Thin Capitalization, Karakteristik Eksekutif dan Multinationality Terhadap Praktik Tax Avoidance. Jurnal Ilmiah MEA (Manajemen, Ekonomi, Dan Akuntansi), 9(1), 1439–1456.

Nyman, R. C. S., Kaidun, I. P., & Lingga, I. S. (2022). Pengaruh Firm Size, Return On Equity, dan Current Ratio Terhadap Tax Avoidance pada Perusahaan LQ 45 yang Terdaftar di Bursa Efek Indonesia. Jurnal Akuntansi, 14(1). https://doi.org/10.28932/jam.v14i1.4375

Prajitno, V. J., Widianingsih, L. P., Jaby, A. C., Hallen, S. I. I., & Pangestu, G. A. (2025). CSR Disclosure and Financial Distress as Determinants of Tax Avoidance: Empirical Evidence from Mining Companies in Indonesia. Ecopreneur.12, 8(2), 148–155. https://doi.org/doi.org/10.51804/econ12.v8i2.148-155

Rahmawati, D., & Nani, D. A. (2021). Pengaruh Profitabilitas, Ukuran Perusahaan, dan Tingkat Hutang Terhadap Tax Avoidance. Jurnal Akuntansi Dan Keuangan, 26(1), 1–11. https://doi.org/10.23960/jak.v26i1.246

Rahmayani, M. W., Hernita, N., & Riyadi, W. (2023). Company Size and Profitability Against Tax Avoidance in Coal Sector Mining Companies Listed on the IDX in 2018-2021. International Journal of Professional Business Review, 8(8). https://doi.org/10.26668/businessreview/2023.v8i8.3262

Rosmanidar, E., Putriana, M., & Nasution, M. A. P. (2024). Pengaruh Biaya Lingkungan Dan Kinerja Lingkungan Terhadap Kinerja Keuangan. E-Bisnis : Jurnal Ilmiah Ekonomi Dan Bisnis, 17(1), 111–125. https://doi.org/10.51903/e-bisnis.v17i1.1770

Sari, P. I. P., & Ramli, A. (2023). The Effect Of Leverage, Company Size, Company Risk On Tax Avoidance In 2020-2022. Jurnal Ilmiah Akuntansi Kesatuan, 11(3). https://doi.org/10.37641/jiakes.v11i3.2074

Septriani, D., & Arianti, B. F. (2025). Pengaruh Struktur Modal, Risiko Perusahaan dan Pertumbuhan Penjualan Terhadap Penghindaran Pajak. JURNAL AKUNTANSI BARELANG, 9(2), 12.

Situmorang, Y. D., Hamzani, U., & Dosinta, N. F. (2025). Determinants of Tax Avoidance on Basic Materials Companies. Jurnal Ilmiah Akuntansi Kesatuan, 13(4), 1063–1074. https://doi.org/10.37641/jiakes.v13i4.3659

Sumartono, S., & Puspasari, I. W. T. (2021). Determinan Tax Avoidance: Bukti Empiris pada Perusahaan Publik di Indonesia. Jurnal Ilmiah Akuntansi, 6(1). https://doi.org/10.23887/jia.v6i1.29281

Susilowati, E., Fadilah, A. K. W., Putri, S. Y., Andayani, S., & Kirana, N. W. I. (2024). Maximizing Firm Value: Analyzing Profitability and Leverage with Tax Avoidance Interventions. Journal of Accounting and Strategic Finance, 7(1). https://doi.org/10.33005/jasf.v7i1.450

Tempo.co. (2024, June 4). PT Antam Diduga Pernah Hindari Pajak Impor Emas yang Didatangkan dari Hong Kong Melalui Singapura, Begini Modusnya. Https://Www.Tempo.Co/Hukum/Pt-Antam-Diduga-Pernah-Hindari-Pajak-Impor-Emas-Yang-Didatangkan-Dari-Hong-Kong-Melalui-Singapura-Begini-Modusnya-52735.

Wibowo, R. Y. K., Asyik, N. F., & Bambang, S. (2021). Pengaruh Struktur Kepemilikan, Arus Kas Bebas, Ukuran Perusahan Terhadap Nilai Perusahaan Melalui Struktur Modal. EKUITAS (Jurnal Ekonomi Dan Keuangan), 5(3). https://doi.org/10.24034/j25485024.y2021.v5.i3.4799

Yohanes, & Sherly, F. (2022). Pengaruh Profitability, Leverage, Audit Quality, dan Faktor Lainnya Terhadap Tax Avoidance. E-Jurnal Akuntansi TSM, 2(2).

Yulianty, R., & Sumanti, E. (2025). Pengaruh Financial Distress Terhadap Penghindaran Pajak Pada Perusahaan Transportasi Yang Terdaftar di Bursa Efek Indonesia Selama Pandemi COVID-19. Journal of Accounting and Finance Management, 6(2). https://doi.org/10.38035/jafm.v6i2.1899