The Role of Corporate Risk as a Moderating Variable: The Effect of Transfer Pricing and Capital Intensity on Tax Aggressiveness

Bilah Samping Artikel

Isi Artikel Utama

Abstrak

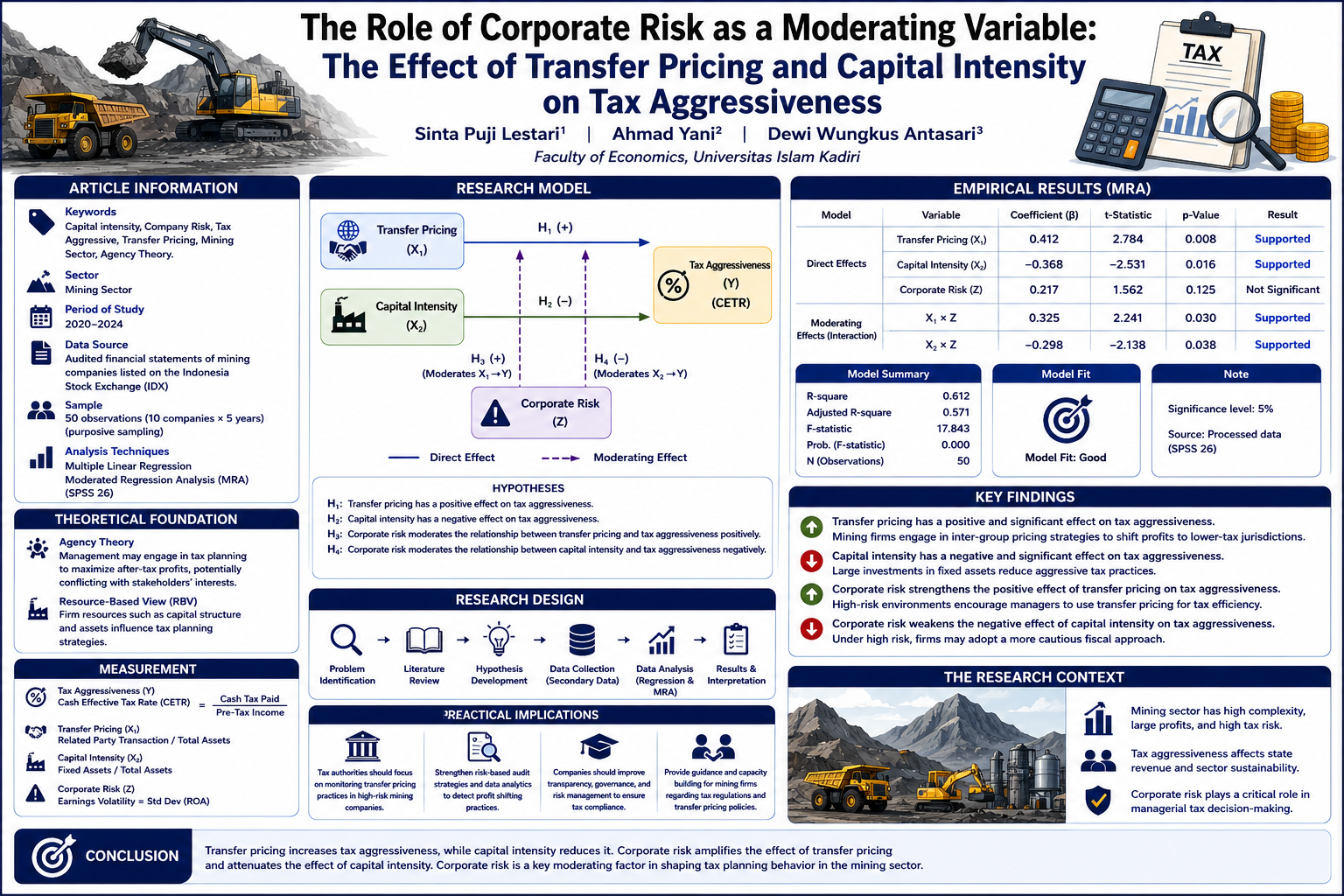

This study aims to investigate the determinants of tax aggressiveness within the mining sector, specifically focusing on the roles of transfer pricing and capital intensity, with corporate risk as a moderating variable. Tax aggressiveness remains a critical issue in the mining industry due to high resource complexity and significant opportunities for profit shifting. Utilizing a quantitative descriptive approach, secondary data were extracted from the audited financial statements of mining companies listed on the Indonesia Stock Exchange (IDX) for the period 2020–2024. Through the application of purposive sampling, a final dataset of 50 observations was obtained. The analytical framework employs Multiple Linear Regression and Moderated Regression Analysis (MRA) to test the hypothesized relationships. The empirical findings reveal that transfer pricing exerts a significant positive effect on tax aggressiveness, suggesting that multinational mining firms frequently utilize inter-group pricing mechanisms to shift profits to lower-tax jurisdictions. Conversely, capital intensity demonstrates a significant negative effect, indicating that substantial investments in fixed assets—characterized by high transparency and strict regulatory depreciation schedules—tend to limit aggressive tax maneuvers. Furthermore, the moderation analysis highlights that corporate risk significantly amplifies the impact of transfer pricing, as high-risk environments incentivize management to prioritize tax efficiency as a buffer against volatility. In contrast, corporate risk attenuates the influence of capital intensity, reflecting a more cautious fiscal approach when operational risks are elevated. The study’s primary novelty resides in positioning corporate risk as a pivotal moderating factor that modulates managerial decision-making. These results provide strategic insights for tax authorities to enhance oversight in high-risk sectors and contribute to the academic discourse on agency-related tax planning.

##plugins.themes.bootstrap3.displayStats.downloads##

Rincian Artikel

Terbitan

Bagian

Artikel ini berlisensi Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Referensi

Adira, N. R., & Tanjung, J. (2025). Pengaruh Likuiditas, Leverage, Komite Audit, dan Capital Intensity Terhadap Agresivitas Pajak: Studi Pada Perusahaan Makanan dan Minuman Terdaftar di BEI. Equilibrium: Jurnal Ilmiah Ekonomi, Manajemen Dan Akuntansi, 14(1), 185–200.

Andini, N. A., Zakaria, A., & Sumiati, A. (2025). Pengaruh Transfer Pricing, Intensitas Aset Tetap, dan Pertumbuhan Penjualan Terhadap Agresivitas Pajak dengan Profitabilitas sebagai Variabel Moderasi. Jurnal Ekonomi Dan Manajemen, 2(2b),4517–4535. https://doi.org/10.62710/cy5yv790

Anggraeni, A. F., Zai, E., & Roswinna, W. (2025). Transfer Pricing, Ukuran Perusahaan, dan Agresivitas Pajak: Studi pada Sektor Pertambangan yang Terdaftar di Bursa Efek Indonesia. Reviu Akuntansi Dan Bisnis Indonesia, 9(2), 421–437. https://doi.org/10.18196/rabin.v9i2.25930

Ayem, S., & Tarang, T. M. D. (2022). Pengaruh Risiko Perusahaan, Kepemilikan Institusional, dan Strategi Bisnis Terhadap Tax Avoidance. Jurnal Riset Akuntansi Dan Keuangan, 17(2). https://doi.org/10.21460/jrak.2021.172.400

Dharmawan, P. E., Djaddang, S., & Darmansyah. (2017). Determinan Penghindaran Pajak Dengan Corporate Social Responsibility Sebagai Variabel Moderasi. Jurnal Riset Akuntansi Dan Perpajakan, 4(2), 183–195.

Fadillah, A. N., & Lingga, I. S. (2021). Pengaruh Transfer Pricing, Koneksi Politik dan Likuiditas Terhadap Agresivitas Pajak (Survey Terhadap Perusahaan Pertambangan yang di BEI Tahun 2016-2019). Jurnal Akuntansi, 13(2), 332–343. https://doi.org/10.28932/jam.v13i2.4012

Hartati, D., & Husnul, N. R. I. (2024). Pengaruh Ukuran Perusahaan, Intensitas Modal, Dan Risiko Perusahaan Terhadap Penghindaran Pajak. Jurnal Akuntansi Keuangan Dan Bisnis, 2(3), 765–770.

Hotimah, L., & Indra, J. (2025). Pengaruh Risiko Perusahaan dan Transfer Pricing dengan Ukuran Perusahaan sebagai Variabel Moderasi. Neraca Akuntansi Manajemen, Ekonomi,23(7).

https://doi.org/10.8734/mnmae.v1i2.359

Jensen, M. C., & Meckling, W. H. (1976). Theory of The Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics, 3(4), 3015–3360.

Kamil, M. I., & Masripah. (2022). Pengaruh Capital Intensity, Risiko Perusahaan, Kompensasi Rugi Fiskal Terhadap Penghindaran Pajak. Akua: Jurnal Akuntansi Dan Keuangan, 1(3), 361–369. https://doi.org/10.54259/akua.v1i3.1033

Margaretha, A., Susanti, M., & Siagian, V. (2021). Pengaruh Deferred Tax, Capital Intensity, dan Return on Asset terhadap Agresivitas Pajak. Jurnal Akuntansi, 13(1), 160–172. https://doi.org/10.28932/jam.v13i1.3537

Marlina, E., Hasanudin, A. I., & Mulyasari, W. (2022). Tax Aggressiveness: The Role of Capital Intensity and Inventory Intensity with Leverage as Intervening. Journal of Applied Business, Taxation and Economics, 1(6),614–632. https://doi.org/10.54408/jabter.v1i6.97

Maulana, T., Keriyanto, Y. W., & Indriyani. (2024). Pengaruh Profitabilitas, Capital Intensity dan Leverage terhadap Effective Tax Rate. Jurnal Ilmu Ekonomi Manajemen Dan Akuntansi MH Thamrin, 5(1), 234–248. https://journal.thamrin.ac.id/index.php/ileka/article/view/2205

Puhowanto. (2025, September). PT. Merdeka Copper Gold Diduga Manipulasi Pajak. SuaraIndonesia1.Com. https://www.suaraindonesia1.com/2025/09/pt-merdeka-copper-gold-diduga.html

Ramadhan, F. A., & Purnamasari, D. (2025). Pengaruh Transfer Pricing, Profitabilitas, dan Leverage Terhadap Penghindaran Pajak (Studi Empiris Pada Perusahaan Coal Production Yang Terdaftar Di BEI 2019-2023). Owner: Riset & Jurnal Akuntansi,9(2). https://doi.org/10.33395/owner.v9i2.2716

Rizkia, W., & Utami, T. (2023). Pengaruh Pertumbuhan Penjualan, Intensitas Aset Tetap, dan Risiko Perusahaan Terhadap Penghindaran Pajak. Akua: Jurnal Akuntansi Dan Keuangan, 2(4), 302–310. https://doi.org/10.54259/akua.v2i4.2064

Safira, M. A., Sodik, & Wahyudi, U. (2024). Pengaruh Transfer Pricing, Tunneling Incentive dan Profitabilitas terhadap Effective Tax Rate Rasio (ETR). Jurnal Economina, 3(6). https://doi.org/10.55681/economina.v3i6.1342

Sari, M. R., & Indrawan, I. G. A. (2022). Pengaruh Kepemilikan Institusional, Capital Intensity, dan Inventory Intensity Terhadap Tax Avoidance. Owner: Riset & Jurnal Akuntansi, 6(4), 4037–4049. https://doi.org/10.33395/owner.v6i4.1092

Setyaningsih, F., Nuryati, T., Rossa, E., & Machdar, N. M. (2023). Pengaruh Profitabilitas, Leverage, dan Capital Intensity Terhadap Tax Avoidance. Sinomika Journal, 2(1), 35–41. https://doi.org/10.54443/sinomika.v2i1.983

Siahaya, P., & Lingga, I. S. (2024). Pengaruh Transfer Pricing Terhadap Agresivitas Pajak di Perusahaan Multinasional. Jurnal Akuntansi, Keuangan, Perpajakan Dan Tata Kelola, 1(4), 441–448. https://doi.org/10.59407/jakpt.v1i4.872

Situmorang, R. (2025). The Effect of Transfer Pricing, Profitability, and Fixed Asset Intensity on Tax Aggresiveness with Audit Commite as Moderating Variable. Indonesian Interdisciplinary Journal of Sharia Economics (IIJSE), 8, 3622–3642.

Soelistiono, S., & Adi, P. H. (2022). Pengaruh Leverage, Capital Intensity, dan Corporate Social Responsibility terhadap agresivitas pajak. Jurnal Ekonomi Modernisasi, 18(1), 38–51. https://doi.org/10.21067/jem.v18i1.6260

Sutrisno, M., & Setyarini, Y. (2024). Pengaruh Profitabilitas, Leverage, Capital Intensity, dan Struktur Kepemilikan Terhadap Agresivitas Pajak Pada Perusahaan Teknologi di BEI. Jurnal of Management and Accounting, 7(2), 259–274. https://doi.org/10.52166/j-macc.v7i2.7717

Utami, M. F., & Irawan, F. (2022). Pengaruh Thin Capitalization dan Transfer Pricing Aggressiveness terhadap Penghindaran Pajak dengan Financial Constraints sebagai Variabel Moderasi. Owner: Riset Dan Jurnal Akuntansi, 6(1), 386–399. https://doi.org/10.33395/owner.v6i1.607

Wardani, D. K., & Dawa, M. E. T. (2022). Pengaruh Corporate Governance Terhadap Penghindaran Pajak dengan Risiko Perusahaan sebagai Variabel Intervening. Jurnal Pendidikan Dasar Dan Sosial Humaniora, 1(10).

Widiyah, E., Abbas, D. S., & Hidayat, I. (2025). Pengaruh Kepemilikan Manajerial, Corporate Social Responsibility, Capital Intensity, dan Ceo Overconfidence Terhadap Agresivitas Pajak. Owner: Riset & Jurnal Akuntansi, 9(3), 1690–1705. https://doi.org/10.33395/owner.v9i3.2747

Yahya, A., Agustin, E. G., & Nurastuti, P. (2022). Firm Size, Capital Intensity dan Inventory Intensity terhadap Agresivitas Pajak. Jurnal Eksplorasi Akuntansi, 4(3), 574–588.