The Effect of Digital Tax Services on MSME Taxpayer Compliance with Tax Literacy as Moderator

Article Sidebar

Main Article Content

Abstract

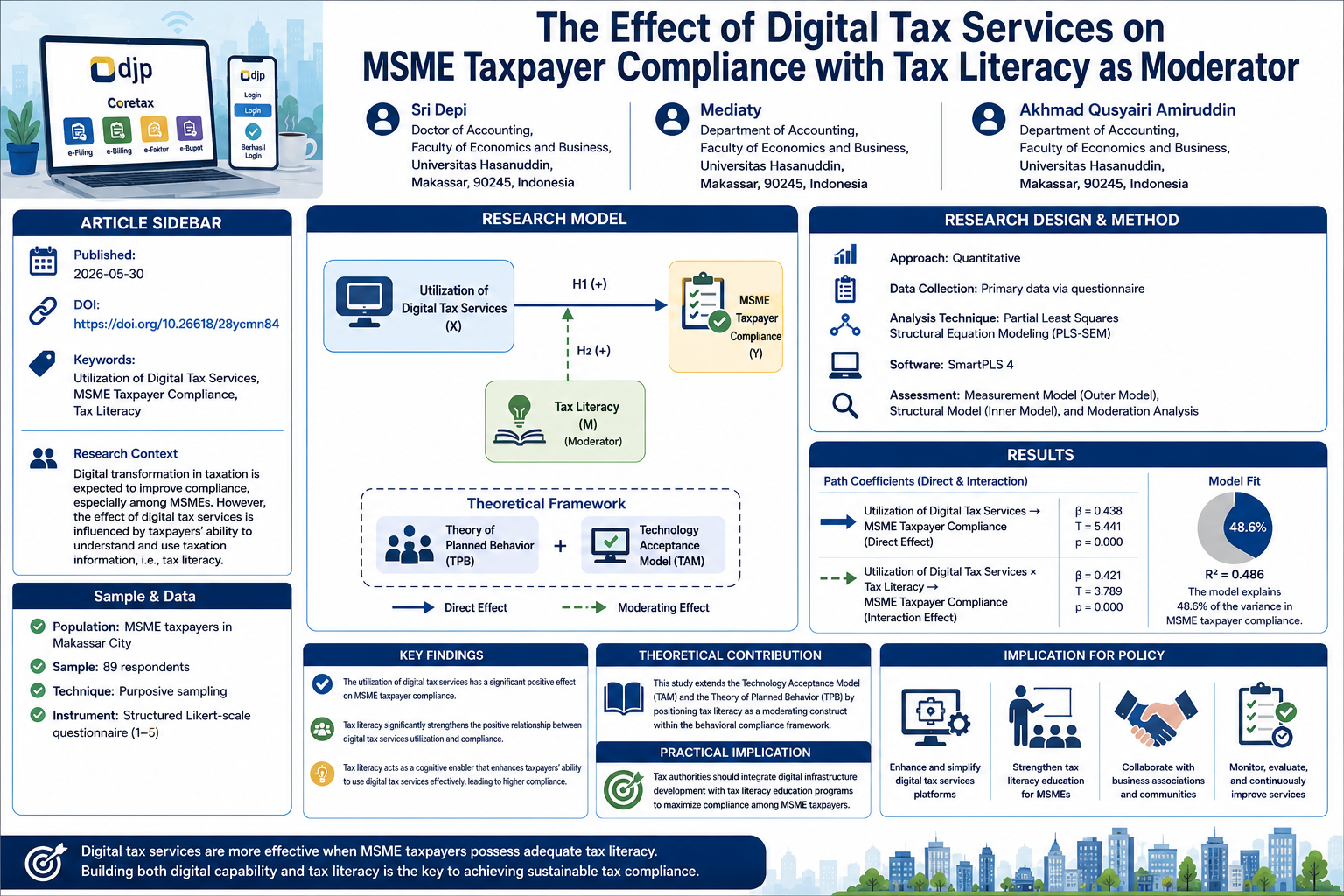

The increasing adoption of digital tax services has raised important questions regarding their effectiveness in encouraging taxpayer compliance, particularly among Micro, Small, and Medium Enterprises (MSMEs) whose engagement with the digital fiscal system is influenced by technological factors and tax literacy. This study aims to analyze the effect of digital tax service utilization on MSME taxpayer compliance in Makassar City, with tax literacy as a moderating variable. A quantitative design was employed, with data collected from 89 MSME taxpayers registered at the local Tax Service Office through a structured Likert-scale questionnaire using a purposive sampling technique. Partial Least Squares Structural Equation Modeling (PLS-SEM) through SmartPLS 4 was applied to assess both direct and interaction effects of moderation. The results reveal that the utilization of digital tax services has a significant positive effect on MSME taxpayer compliance (β = 0.438, T = 5.441, p = 0.000), and that tax literacy significantly moderates this relationship (β = 0.421, T = 3.789, p = 0.000), with the model explaining 48.6% of the variance in compliance. These findings extend the Technology Acceptance Model and the Theory of Planned Behavior by demonstrating that tax literacy strengthens the compliance-enhancing impact of digital tax platforms, serving as a critical cognitive enabler for MSME taxpayers. This study contributes theoretically by positioning tax literacy as a moderating construct within the behavioral compliance framework, and practically by recommending an integrated policy strategy that combines digital infrastructure development with tax literacy education programs to maximize compliance outcomes among MSME taxpayers.

Downloads

Article Details

Section

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

Abu-Silake, S.A., Alshurafat, H., Alaqrabawi, M., & Shehadeh, M. (2024). Exploring the key factors influencing the actual usage of digital tax platforms. Discover Sustainability, 5 (1), 88. https://doi.org/10.1007/s43621-024-00241-2

Agostino, D., Saliterer, I., & Steccolini, I. (2022). Digitalization, accounting and accountability: A literature review and reflections on future research in public services. Financial Accountability & Management, 38 (2), 152–176. https://doi.org/10.1111/faam.12301

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50 (2), 179–211.

Alm, J., & Torgler, B. (2011). Do ethics matter? Tax compliance and morality. Journal of Business Ethics, 101 (4), 635–651.

Bassey, E., Mulligan, E., & Ojo, A. (2022). A conceptual framework for digital tax administration—A systematic review. Government Information Quarterly , 39 (4), 101754. https://doi.org/10.1016/j.giq.2022.101754

Belahouaoui, R., & Attak, E. H. (2024). Digital taxation, artificial intelligence and Tax Administration 3.0: Improving tax compliance behavior – a systematic literature review using textometry (2016–2023). Accounting Research Journal, 37 (2), 172–191. https://doi.org/10.1108/ARJ-12-2023-0372

Bhushan, P., & Medury, Y. (2014). Empirical Study of Financial and Tax Literacy of Salaried Individuals.

Buchan, M. C., Bhawra, J., & Katapally, T. R. (2024). Navigating the digital world: Development of an evidence-based digital literacy program and assessment tool for youth. Smart Learning Environments, 11 (1), 8. https://doi.org/10.1186/s40561-024-00293-x

Davis, F.D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13 (3), 319–340.

De Clercq, B. (2023). Tax literacy: What does it mean? Meditari Accountancy Research, 31 (3), 501–523. https://doi.org/10.1108/MEDAR-04-2020-0847

DeLone, W. H., & McLean, E. R. (2003). The DeLone and McLean model of information systems success: A ten-year update. Journal of Management Information Systems, 19 (4), 9–30.

Diantini, A., Yasa, INP, & Atmadja, AT (2018). The effect of e-filing implementation on individual taxpayer compliance (Study at Singaraja Primary Tax Service Office). JIMAT (Scientific Journal of Accounting Students) Undiksha, 9 (1).

Heinemann, M., & Stiller, W. (2025). Digitalization and cross-border tax fraud: Evidence from e-invoicing in Italy. International Tax and Public Finance, 32 (1), 195–237. https://doi.org/10.1007/s10797-023-09820-x

Hesami, S., Jenkins, H., & Jenkins, G. P. (2024). Digital Transformation of Tax Administration and Compliance: A Systematic Literature Review on E-Invoicing and Prefilled Returns. Digital Government: Research and Practice, 5 (3), 1–20. https://doi.org/10.1145/3643687

Idrus, M. (2024). Efficiency of tax administration and its influence on taxpayer compliance. Economics and Digital Business Review, 5 (2), 889–913.

Kebede, TN, Ethiopian Federal Democratic Republic Ministry of Revenue, Hawassa Branch, Hawassa City, Ethiopia, Fitamo, TL, & College of Business and Economics, Hawassa University, Hawassa, Ethiopia. (2025). Practice, Opportunities, and Challenges of Electronic Tax Systems from Taxpayer's Perspective: Evidence from Ethiopia. Journal of Tax Reform, 11 (1), 6–24. https://doi.org/10.15826/jtr.2025.11.1.189

Kirchler, E. (2007). The economic psychology of tax behavior. Cambridge university press.

Kristanto, MVA, Nurhasanah, F., Setiawan, R., & Shahrill, M. (2025). Mathematics Instruction as a Bridge for Elevating Students' Financial Literacy: Insight from a Systematic Literature Review. Open Education Studies, 7 (1), 20250112.

Loo, E.C., Evans, C., & McKerchar, M.A. (2012). Challenges in understanding compliance behavior of taxpayers in Malaysia. Asian Journal of Business and Accounting, 3 (2), 2010.

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and Evidence. Journal of Economic Literature, 52 (1), 5–44.

Mosca, O., Manunza, A., Manca, S., Vivanet, G., & Fornara, F. (2024). Digital technologies for behavioral change in sustainability domains: A systematic mapping review. Frontiers in Psychology, 14, 1234349. https://doi.org/10.3389/fpsyg.2023.1234349

Mujiyati, M., Zulfikar, Z., Witono, B., & Cahyo Utomo, I. (2024). The impact of digital platforms in tax administration services on local government tax revenues: Evidence from Indonesia. Public and Municipal Finance, 13 (2), 195–203. https://doi.org/10.21511/pmf.13(2).2024.16

Mukhlis, I., Utomo, SH, & Soesetio, Y. (2015). The role of taxation education on taxation knowledge and its effect on tax fairness as well as tax compliance on handicraft SMEs sectors in Indonesia. International Journal of Financial Research, 6 (4), 161–169.

Nzioki, P., & Peter, O.R. (2014). Analysis of factors affecting tax compliance in real estate sector: A case of real estate owners in Nakuru Town, Kenya. Research Journal of Finance and Accounting, 5 (11), 1–12.

Rizkina, M. (2025). Reinventing Central Tax Administration: A Systematic Literature Review on Digital Tax Transformation and Compliance Enhancement in 2020–2025. Action Research Literate, 9 (12). https://doi.org/10.46799/arl.v9i12.3072

Roida, Rini Werdiningsih, & Emiliana Sri Pudjiarti. (2025). The Implementation of Tax Administration Digitalization Policy on Tax Compliance in Manufacturing Industry Companies. Social Dynamics: International Journal of Social Sciences and Communication, 1 (3), 45–54. https://doi.org/10.70062/dynamicssocial.v1i3.231

Rokhman, A., Handoko, W., Tobirin, T., Antono, A., Kurniasih, D., & Sulaiman, AI (2023). The effects of e-government, e-billing and e-filing on taxpayer compliance: A case of taxpayers in Indonesia. International Journal of Data and Network Science, 7 (1), 49–56.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers' view. Procedia-Social and Behavioral Sciences, 109, 1069–1075.

Sari, NWSD (2024). Implications of Tax Digitalization, Tax Understanding, Tax Sanctions and Taxpayer Trust in Taxpayer Compliance in Bali.

Sholihah, A., & Nugroho, L. (2025). Beyond Tax Knowledge: Exploring the Impact of Digital Literacy and Tax Stereotypes on MSME Tax Compliance (Case Study on MSME Taxpayers in Kesambi District, Cirebon, West Java, Indonesia). Business, Management & Accounting Journal (BISMA), 2 (1), 1–14.

Sijabat, R. (2020). Analysis of e-Government Services: A Study of the Adoption of Electronic Tax Filing in Indonesia. Journal of Social and Political Sciences, 23 (3), 179. https://doi.org/10.22146/jsp.52770

Umbet, M., Askarov, D., Rudžionienė, K., Christauskas, Č., & Alikulova, L. (2025). Evaluating the Implementation of Information Technology Audit Systems Within Tax Administration: A Risk Governance Perspective for Enhancing Digital Fiscal Integrity. Journal of Risk and Financial Management, 18 (8), 422. https://doi.org/10.3390/jrfm18080422

Widianti, E. (2025). The Role of Tax Sanctions in Shaping Taxpayer Behavior in MSMEs: A Literature Review Study. Journal of Business Economics and Entrepreneurship, 2 (4), 19–26. https://doi.org/10.69714/jvztcc68