Evaluating the Effectiveness of Surface Water Tax Collection Mechanisms: A Case Study of the Samsat Office in Gowa Regency

Article Sidebar

Main Article Content

Abstract

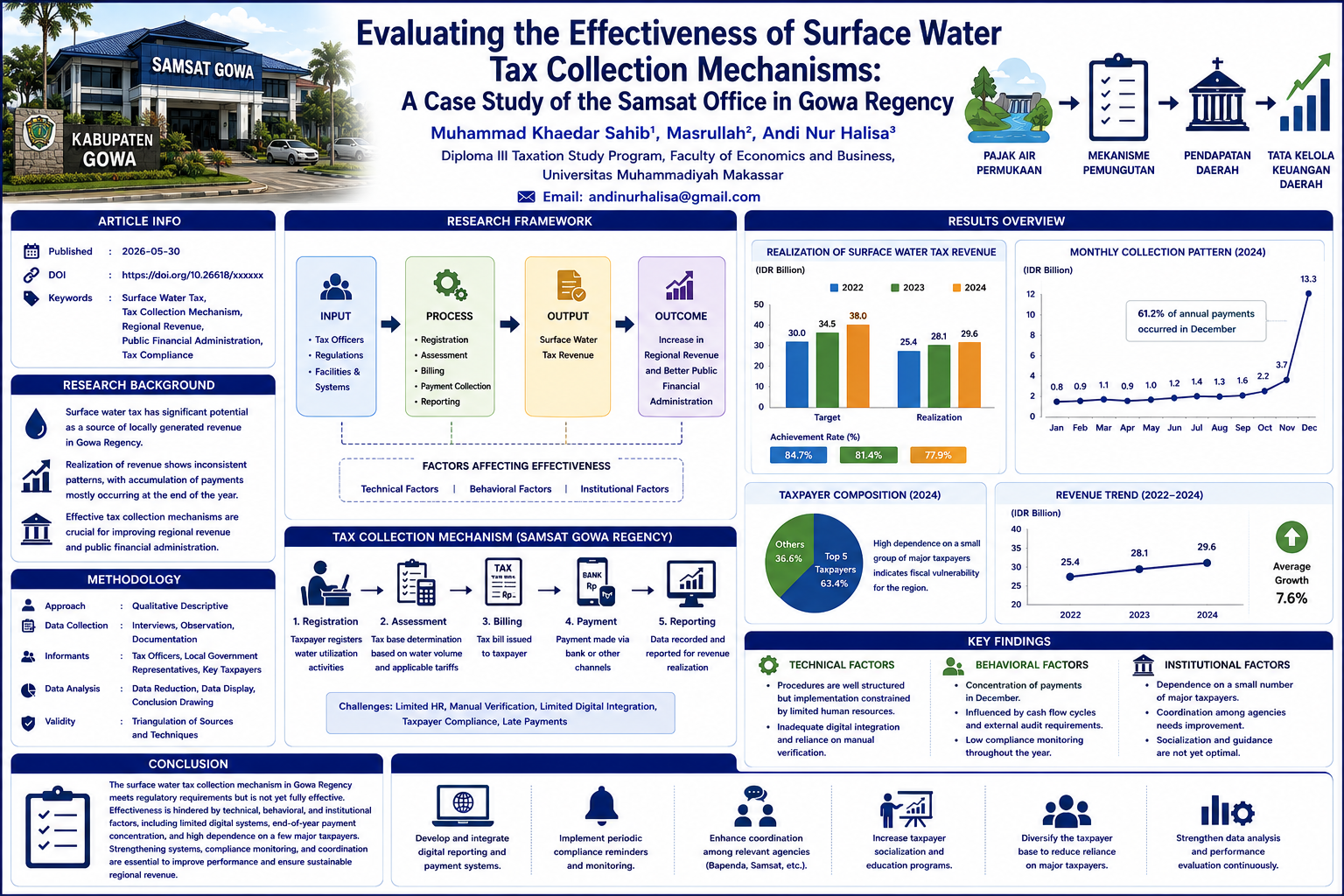

This study examines the effectiveness of surface water tax collection mechanisms implemented by the Samsat Office of Gowa Regency, Indonesia, in the context of increasing regional revenue demands and the need for efficient public financial administration. Despite the significant potential of surface water taxation as a source of locally generated revenue, its realization has shown inconsistent patterns, particularly the recurring accumulation of payments near the end of the fiscal year. Using a qualitative descriptive approach, data were collected through interviews, observation, and documentation involving tax officers, local government representatives, and key taxpayers. The analysis reveals several key findings. First, administrative procedures for tax assessment and billing are generally well structured; however, operational implementation remains constrained by limited human resources, inadequate digital integration, and dependence on manual verification. Second, the concentration of payments in December is influenced by taxpayer behavior, corporate cash flow cycles, and external audit requirements, indicating structural weaknesses in periodic monitoring. Third, the tax revenue structure is highly dependent on a small group of major taxpayers, posing fiscal vulnerability for the region. Overall, while the tax collection mechanism meets regulatory requirements, its effectiveness is hindered by technical, behavioral, and institutional factors. The study recommends strengthening digital reporting systems, implementing periodic compliance reminders, enhancing inter-agency coordination, and diversifying the taxpayer base to ensure sustainable regional revenue.

Downloads

Article Details

Section

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

Mafaza, W., Mayowan, Y., & Sasetiadi, T. H. (2016). Kontribusi Pajak Daerah dan Retribusi Daerah dalam Pendapatan Asli Daerah. Jurnal Perpajakan (JEJAK), 11(1).

Mardiasmo. (2009). Perpajakan (Edisi Revisi). Yogyakarta: CV Andi.

Mardiasmo. (2016). Perpajakan (Edisi Terbaru). Yogyakarta: Andi.

Mardiasmo. (2018). Perpajakan (Edisi Terbaru). Jakarta: Andi.

Purnamawati, E. (2017). Pemungutan Pajak di Indonesia. Jurnal Fakultas Hukum Universitas Palembang, 15(3), 342–437.

Republik Indonesia. (2007). Undang-Undang Nomor 28 Tahun 2007 tentang Ketentuan Umum dan Tata Cara Perpajakan.

Republik Indonesia. (2009). Undang-Undang Nomor 28 Tahun 2009 tentang Pajak Daerah dan Retribusi Daerah.

Republik Indonesia. (2009). Undang-Undang Nomor 16 Tahun 2009 tentang Ketentuan Umum dan Tata Cara Perpajakan.

Ropah, T., Alexander, S. W., & Mintalangi, S. S. (2021). Evaluasi Penerapan Perhitungan, Penetapan dan Pembayaran Pajak Air Permukaan pada PT Air Manado. Going Concern: Jurnal Riset Akuntansi, 16(3), 209–216.

Rusjdi, M. (2007). Pajak Pertambahan Nilai dan Pajak Penjualan. Jakarta: PT Gramedia Pustaka Utama.

Siahaan, M. P. (2013). Pajak Daerah dan Retribusi Daerah (Edisi Revisi). Jakarta: Raja Grafindo Persada.

Soemitro, R. (2007). Dasar-dasar Hukum Pajak dan Pendapatan. Bandung: Eresco.

Sumarsan, T. (2017). Perpajakan Indonesia (Edisi Kelima). Jakarta: Indeks.

Waluyo, & Ilyas, W. B. (2008). Perpajakan Indonesia (Edisi Revisi). Jakarta: Salemba Empat.

Pemerintah Provinsi Sulawesi Selatan. (2010). Peraturan Daerah Provinsi Sulawesi Selatan Nomor 10 Tahun 2010 tentang Pajak Daerah dan Retribusi Daerah.

Ghozali, I. (2016). Aplikasi Analisis Multivariate dengan Program IBM SPSS 23. Semarang: Badan Penerbit Universitas Diponegoro.

Sugiyono. (2019). Metode Penelitian Kuantitatif, Kualitatif, dan R&D. Bandung: Alfabeta.

Creswell, J. W. (2014). Research Design: Qualitative, Quantitative, and Mixed Methods Approaches (4th ed.). Thousand Oaks, CA: Sage Publications.

Undang-Undang Republik Indonesia Nomor 23 Tahun 2014 tentang Pemerintahan Daerah.

Undang-Undang Republik Indonesia Nomor 33 Tahun 2004 tentang Perimbangan Keuangan antara Pemerintah Pusat dan Pemerintahan Daerah.